Treasury’s first GENIUS rule tightens Washington’s grip on who can scale stablecoins

Treasury’s first proposed rule under the GENIUS Act does more than outline stablecoin supervision, as it shows where control sits as the market scales: states may license issuers early, but Washington sets the terms that matter once stablecoins become large enough to matter to the dollar system.

Treasury's first proposed GENIUS rule landed on April 1 as a notice of proposed rulemaking.

The text inside it builds the operational architecture for US stablecoin governance, addressing which institutions may issue payment stablecoins, under what conditions, and at what scale before federal oversight becomes mandatory.

Why this matters: Treasury is drawing a harder line between small issuers and systemically relevant ones. That matters because stablecoins are no longer a niche crypto product. They are becoming part of dollar payments, liquidity, and treasury infrastructure, which means the rules now shape who can scale, who gets squeezed, and how concentrated the market may become.

By defining when a state licensing regime qualifies as “substantially similar” to the federal framework, Treasury is now defining those terms.

The stablecoin market already holds roughly $316 billion, with USDT accounting for about 58% of the supply, per DeFiLlama.

Retail-sized volume for USDC, USDT, and PYUSD grew from $500 million to $69.8 billion between 2019 and 2025. FSOC's 2025 annual report described the GENIUS framework as a federal prudential system designed to onshore stablecoin innovation, protect holders in the event of insolvency, and support the US dollar's international role.

Treasury's NPRM now shows how that prudential vision operates on the ground.

The hidden fight over who governs

The Treasury chairs the interagency review committee that certifies state stablecoin regimes, which includes leadership from the Fed and the FDIC.

That committee's judgment rests on the “substantially similar” test, and Treasury's proposal defines that test to include the GENIUS Act itself, as well as the implementing regulations and interpretations issued by federal agencies over time.

Treasury says that substantial similarity would be hard to administer, and state and federal standards could “starkly deviate.”

As OCC, Treasury, the Fed, FinCEN, and OFAC add implementing rules, the standard Washington uses to measure states shifts with them. State regimes approved today must track a benchmark that Washington keeps building.

Treasury organizes the rule around two categories. The first, called uniform, covers the parts that establish trust in the instrument itself: reserve assets, redemption, monthly reserve publication, limits on rehypothecation, accountant examinations, BSA/sanctions compliance, lawful-order capability, and core activity limits.

State implementation of each uniform requirement must be consistent with the federal framework “in all substantive respects,” with no material deviations in definitions or scope. For BSA and sanctions specifically, states must cross-reference federal rules directly, with no room for state-drafted substitutes.

The second category allows calibration around some capital, liquidity, reserve diversification, risk management, applications, licensing, and certain redemption mechanics. Treasury still constrains that room, and state choices in the flexible bucket must produce outcomes “at least as stringent and protective” as the federal framework.

For example, a state may allow additional reserve assets only if the OCC has already approved them as similarly liquid federal government-issued assets. That is federal pre-clearance administered through state paperwork.

| Category | Requirement area | Treasury standard | State discretion | Why it matters |

|---|---|---|---|---|

| Uniform | Reserve assets | Must align with the federal framework in all substantive respects | No material deviation | Defines trust in the stablecoin itself |

| Uniform | Redemption | Must track the federal baseline closely | No narrower state substitute | Protects holders’ ability to redeem |

| Uniform | Monthly reserve publication | Must match federal expectations | Very limited room to vary | Supports transparency and market confidence |

| Uniform | Limits on rehypothecation | Must conform to the federal framework | No meaningful carve-out | Prevents riskier use of backing assets |

| Uniform | Accountant examinations | Must be consistent with federal requirements | Little to no variation | Standardizes verification of reserves |

| Uniform | BSA / AML / sanctions | States must cross-reference federal rules directly | No state-drafted alternative | Keeps compliance under national control |

| Uniform | Lawful-order capability | Must track federal expectations | Minimal discretion | Preserves enforcement and legal access |

| Uniform | Core activity limits | Must align with the federal framework | No material divergence | Keeps issuers inside a nationally defined model |

| Flexible / calibrated | Capital | Outcomes must be at least as stringent and protective as the federal framework | Some calibration allowed | Lets states tune prudential standards without weakening them |

| Flexible / calibrated | Liquidity | Must be at least as protective as the federal baseline | Some calibration allowed | Gives limited room for state tailoring |

| Flexible / calibrated | Reserve diversification | May vary, but only within outcomes at least as protective as the federal framework | Narrow flexibility | States can adjust, but not create a looser reserve regime |

| Flexible / calibrated | Risk management | State framework can differ in form | Must still meet protective federal-equivalent outcomes | Allows administrative variation, not a different philosophy |

| Flexible / calibrated | Applications / licensing | State administration is allowed | Cannot create a genuinely different regime | Keeps the state lane administrative, not alternative |

| Flexible / calibrated | Certain redemption mechanics | Some room to calibrate | Must remain at least as protective as the federal system | States can adjust process, not weaken substance |

| Flexible / calibrated | Additional reserve assets | Allowed only if the OCC has already approved comparable assets | Federal pre-clearance still governs | Shows state flexibility is still bounded by Washington |

This is the core shift in plain terms: the state path exists, but only inside a federal design that gets tighter as stablecoins grow. The real question is no longer whether stablecoins will be regulated, but who will still be able to issue them once compliance costs and scale thresholds start to bite.

The $10 billion ceiling and what it produces

The GENIUS Act caps the state option at issuers with no more than $10 billion in consolidated outstanding payment stablecoins.

Treasury adds that state transition rules cannot impede a move to federal oversight once an issuer crosses that line, and issuers in a state that fails certification must either stop issuing payment stablecoins or move into the federal licensing framework.

The $10 billion ceiling is the structural tell, since the state lane functions as an entry point for smaller issuers. At scale, the federal framework becomes the only durable home.

Citi's updated 2026 forecast puts its base-case estimate for the 2030 stablecoin market at $1.9 trillion. Standard Chartered projected the market could reach $2 trillion by the end of 2028.

A market at that scale runs on uniform reserve, redemption, and compliance standards and rewards issuers capable of absorbing national-style regulatory overhead.

Visa's concentration data already reflects the current destination: as of October 2025, more than 97% of the stablecoin supply had converged on USDT and USDC. Treasury's design standardizes the conditions that large, compliant issuers are already built to meet.

Standard Chartered estimated stablecoins could pull roughly $500 billion in deposits out of US banks by the end of 2028.

The number frames the context correctly: stablecoins are becoming claims on dollar liquidity that sit alongside traditional bank deposits, and the institution that governs the terms of stablecoin issuance governs an expanding piece of dollar infrastructure.

Treasury's proposal positions Washington as that institution.

| Scale marker | Amount | What it represents | Regulatory implication | Why it matters |

|---|---|---|---|---|

| State-lane ceiling | $10 billion | Maximum consolidated outstanding payment stablecoins for an issuer to remain in the state option | Above this line, the issuer must transition to federal oversight or stop issuing new payment stablecoins | Shows the state path is a limited entry lane, not the durable home for large issuers |

| Current stablecoin market | ~$316 billion | Approximate current total stablecoin market size | The market is already far larger than the state-lane threshold | Suggests Treasury is designing rules for a systemically meaningful market, not a niche one |

| Citi base case (2030) | $1.9 trillion | Citi’s updated 2026 base-case estimate for the stablecoin market by 2030 | A market at this scale would likely rely on uniform national standards rather than fragmented state variation | Reinforces the article’s argument that scale points toward federalization |

| Standard Chartered forecast (end-2028) | $2 trillion | Standard Chartered’s projection for stablecoin market size by the end of 2028 | Implies that if growth continues, large issuers will almost inevitably end up in the federal framework | Supports the view that the state lane functions more like a launch ramp than a long-term alternative |

| Bank deposit migration estimate | ~$500 billion | Standard Chartered estimate of deposits stablecoins could pull from U.S. banks by end-2028 | Stablecoin issuance becomes a question of dollar-system governance, not just crypto regulation | Helps mainstream readers see this as a financial-architecture story, not a niche policy update |

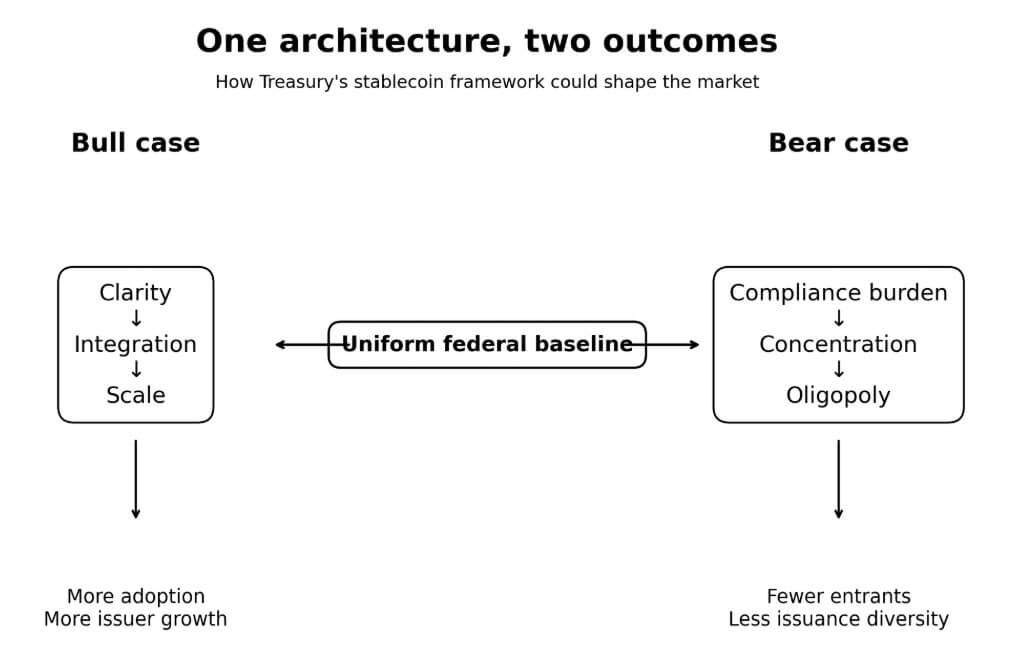

Two paths through the same architecture

The bull case runs from clarity to scale. Uniform national rules on reserves, redemption, and compliance remove the uncertainty that has kept banks, card networks, and enterprise treasury teams cautious about deep integration with stablecoins.

Along that path, supply tracks toward the Citi and Standard Chartered forecasts, Visa's 130-plus card programs are overlaid on stablecoin wallets, and the state lane serves as a launch ramp for smaller issuers before they graduate to federal supervision.

Treasury's tight architecture then reads as the operating manual for US digital dollar expansion, which is a framework that made the market credible enough to absorb institutional demand at scale.

The bear case runs the same architecture in reverse. The forthcoming BSA/AML and lawful order rules, which both Treasury and the OCC have flagged as still pending in separate rulemakings, could entail heavy operational requirements.

If certification proves slow, costly, or politically fraught, smaller issuers may find the state lane functionally inaccessible even before they approach the $10 billion threshold.

The result would be a market that is legally cleaner but structurally oligopolistic, with innovation relocating to distribution and infrastructure, away from issuance.

Treasury frames a different goal. The predictable market response to high uniform compliance floors and a hard ceiling on state-lane scale is concentration, and Visa's existing market data shows the market was already moving in that direction before the rule arrived.

A dual-path diagram shows how Treasury's uniform federal stablecoin baseline could drive either broader adoption or market concentration depending on compliance outcomes.

A dual-path diagram shows how Treasury's uniform federal stablecoin baseline could drive either broader adoption or market concentration depending on compliance outcomes.

Washington holds the baseline

This NPRM is part of a larger regulatory framework. OCC's February proposal covered the required GENIUS regulations, except those tied to BSA, AML, and OFAC sanctions, which will be addressed in a separate rulemaking coordinated with Treasury.

Treasury's own NPRM flags that rules on lawful-order compliance are forthcoming as well. The full compliance map for stablecoin issuers awaits completion.

The $316 billion market and $10 trillion transaction volume settled the question of stablecoins belonging in the US finance. Treasury is deciding who gets to shape them as they enter it.

The next test is not whether Washington wants stablecoins inside the financial system. That question is already settled. The next test is whether the remaining GENIUS rulemakings leave room for more issuers to survive inside that system, or whether the market exits this process cleaner, larger, and far more concentrated than it entered.

The post Treasury’s first GENIUS rule tightens Washington’s grip on who can scale stablecoins appeared first on CryptoSlate.

You May Also Like

The changing face of elder care in Malaysia — Sayed Mohammad Reza Yamani Sayed Umar

Not a loophole: Singapore AI export controls let China tap US AI legally

Exclusive interview with Smokey The Bera, co-founder of Berachain: How the innovative PoL public chain solves the liquidity problem and may be launched in a few months