Intel (INTC) Stock: Q1 Earnings Report and What Wall Street Is Watching

Key Takeaways

- Wall Street anticipates Q1 adjusted earnings per share of $0.02, a significant decline from $0.13 in the prior-year period, with revenues near $12.4 billion

- The foundry division is expected to record a $2.4 billion operating deficit for Q1, currently serving only Intel as a client

- Shares of INTC have skyrocketed 235% year-over-year, recently touching a fresh peak of $70.33, with a forward P/E ratio of 92x

- Intel’s position in the data center market has contracted dramatically from 71% in 2021 to merely 7% in 2024, as Nvidia captured dominant share

- Strategic partnerships with Nvidia, Google, Elon Musk’s Terafab project, and a plant stake repurchase from Apollo are transforming investor sentiment

Intel is scheduled to release its first-quarter financial results Thursday following market close. While the headline figures matter, investors are primarily focused on CEO Lip-Bu Tan’s commentary regarding the company’s progress in securing third-party customers for its foundry operations.

Intel Corporation, INTC

Analysts are projecting Q1 adjusted earnings of $0.02 per share, representing a steep drop from the $0.13 reported during the comparable quarter last year. Revenues are anticipated to reach approximately $12.4 billion, marking a modest 2% year-over-year contraction.

The semiconductor giant’s shares have experienced an extraordinary rally. From bottoming at $17.67 twelve months ago, INTC has climbed 235%, touching a record high of $70.33 in recent sessions. The stock currently commands a forward earnings multiple of 92 — dramatically higher than the S&P 500’s roughly 21x ratio.

This premium valuation isn’t justified by current profitability metrics. Instead, it reflects investor optimism around strategic initiatives and favorable political positioning.

Tan orchestrated a sale of a 9% ownership stake to the U.S. government, securing strong support from the Trump administration. He also forged a strategic alliance with Nvidia that included the AI chipmaker acquiring a 4.5% position in Intel. Subsequently, Intel announced a collaboration with Elon Musk’s ventures to construct the Terafab manufacturing complex in Texas, which will produce semiconductors for SpaceX, xAI, and Tesla.

Additionally, Intel secured a multi-year agreement with Google to deliver AI and inference computing capabilities on Google Cloud utilizing its Xeon processor lineup. In a significant financial maneuver, the company agreed to repurchase a 49% interest in a fabrication facility previously sold to Apollo Global Management in 2024 — paying $14.2 billion for assets it divested for $11.2 billion.

Foundry Operations Remain a Critical Hurdle

The foundry business continues to represent Intel’s primary strategic challenge. Currently, it serves a single client: Intel’s own chip design divisions. Wall Street projects a $2.4 billion operating loss for this segment in Q1.

Tan has emphasized that funding the next-generation manufacturing capabilities will require revenue from external clients. Without third-party customers, the financial model becomes unsustainable.

Intel’s production technology has trailed Taiwan Semiconductor Manufacturing for an extended period, and this technological disadvantage has hindered efforts to attract the major fabless semiconductor companies that constitute TSMC’s customer base. Narrowing this technology gap — or persuading customers to commit despite it — represents the fundamental challenge ahead.

PC Market Softness Creates Additional Headwinds

The Client Computing division, responsible for PC processors, accounts for approximately 57% of estimated Q1 revenues. This business faces headwinds from a worldwide memory component shortage that’s driving up PC prices and suppressing consumer demand.

International Data Corporation forecasts global PC unit shipments will decline 11.3% in 2026, though elevated average selling prices should maintain relatively stable revenue levels. Intel anticipates Client Computing revenues of approximately $7.1 billion for Q1, representing a 7% year-over-year decrease.

On a more positive note, Intel’s Data Center and AI division is projected to generate $4.41 billion in Q1, reflecting 6.8% year-over-year growth. The company identified supply bottlenecks for its data center processors in Q4 but indicated these constraints should diminish following Q1.

The emergence of AI agents — which depend substantially on CPUs for operations including web navigation and data manipulation — is creating renewed demand for Intel’s traditional processor lineup within AI infrastructure deployments.

Intel reported experiencing supply limitations on data center chips during Q4 2025 and anticipates gradual improvement throughout 2026.

The post Intel (INTC) Stock: Q1 Earnings Report and What Wall Street Is Watching appeared first on Blockonomi.

You May Also Like

Teacher accuses MAGA superintendent of working with Libs of TikTok to destroy his career

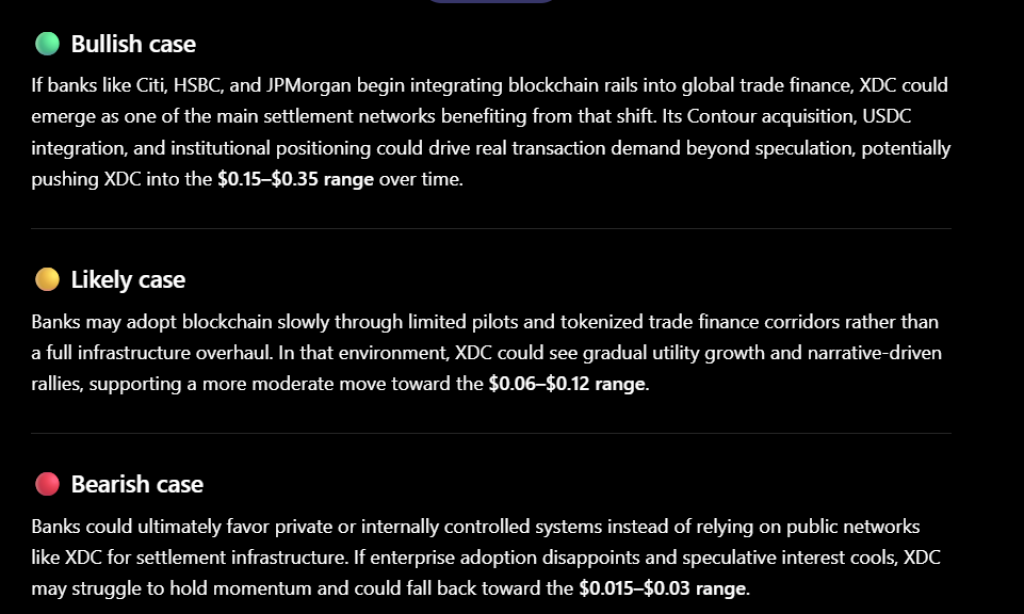

ChatGPT Predicts XDC Network Price if Banks Finally Upgrade the “Plumbing” Behind Global Trade Finance