Upcoming Crypto Token Unlocks: $86.21M in Supply Across 31 Crypto Projects (June 15–21, 2026)

The week of June 15–21, 2026 features scheduled token unlocks for 31 tracked crypto assets, with a combined upcoming unlock value of approximately $86,212,492 (about $86.21M) based on prices as of June 15, 2026, 05:02 AM UTC. Unlock pressure is concentrated in several high‑impact events from ZRO, SPK, KAITO, ARB, SEI, BR, UDS, YZY, and ZK, while a long tail of smaller unlocks adds incremental emissions rather than systemic shocks.

Although the aggregate unlock value is moderate in the context of recent high‑notional weeks, the relative unlock size versus market capitalization and the emission stage (“Released %”) of several mid‑cap and early‑curve tokens still introduces notable short‑term dilution and volatility risk. Compared with broader June 2026 unlock coverage, this week’s schedule is dominated by a handful of large events, particularly ZRO and SPK which anchor the high‑value tier, while ARB, SEI, KAITO, UDS, and BR reinforce the overall unlock profile.

Large infrastructure, DeFi, and ecosystem tokens will be in focus as traders weigh potential selling pressure against prevailing market sentiment, liquidity conditions, and any concurrent protocol or ecosystem catalysts.

Major token unlock events

This week’s top‑tier unlocks are dominated by high‑impact events expected to draw significant market attention and drive event‑driven trading flows.

Major token unlock events (tokenomist)

Major token unlock events (tokenomist)

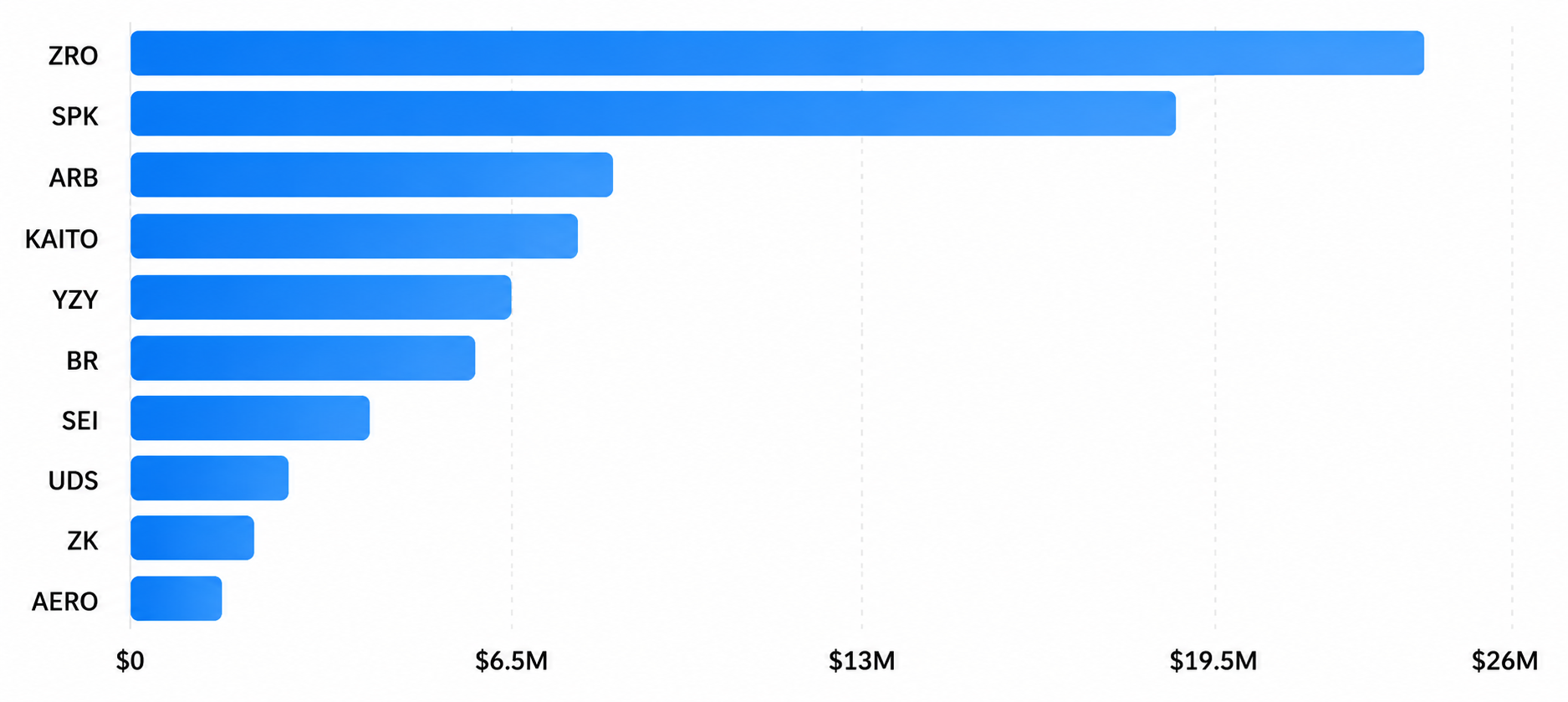

ZRO – $23.16M unlock

ZRO has the largest upcoming unlock of the week at about $23.16M, against a reported market cap of $241.47M and a price of $0.958. With 53.28% of its maximum supply already released, this unlock is substantial in absolute terms and sizable as a percentage of market cap, expanding the circulating float meaningfully in a single week.

ZRO’s emissions remain in a mid-curve phase, making the upcoming ZRO Token Unlock an important event for supply dynamics and investor positioning. Traders will watch closely to see whether the ecosystem can absorb the new tokens without driving a repricing or widening of spreads, especially if derivatives positioning and funding are skewed into the event.

SPK – $18.49M unlock

SPK is set for an unlock of around $18.49M, with a reported market cap of $56.04M and a price of $0.02. Only 33.01% of its supply is currently released, placing SPK in an early‑to‑mid emission stage where new unlocks materially reshape circulating supply.

Because the upcoming unlock value represents a very high fraction of the reported market cap, SPK stands out as one of the highest unlock‑to‑cap ratios on this week’s calendar and one of the clearest short‑term dilution overhangs. Market participants should expect elevated sensitivity to flows around the event, particularly if a significant portion of the unlocked allocation belongs to investors or team wallets.

ARB – $8.04M unlock

ARB faces an unlock of about $8.04M, compared with a reported market cap of $536.43M and a price of $0.086. At 55.21% of supply released, ARB displays a more mature profile than early‑curve names, with emissions that are large in dollar terms but relatively smaller as a fraction of market cap.

As a larger infrastructure‑aligned asset, ARB’s unlock is likely to be absorbed more efficiently than those of smaller caps, but derivatives positioning, liquidity fragmentation across exchanges, and broader L2 sentiment can still amplify short‑term price moves around the event.

KAITO – $7.40M unlock

KAITO is scheduled to unlock approximately $7.40M in tokens, with a reported market cap of $114.35M and a price of $0.474. With 39.19% of supply released, KAITO sits in a mid‑curve emission phase, where unlocks still represent a key structural driver of float expansion.

The upcoming unlock equates to a meaningful share of market cap, making KAITO a key name to monitor for post‑event selling and intraday volatility, especially if spot liquidity and exchange coverage are uneven.

YZY – $6.23M unlock

YZY has an upcoming unlock of around $6.23M on a reported market cap of $38.62M and a price of $0.297, with 48.75% of supply released. This mid‑curve profile combined with a sizeable unlock‑to‑cap ratio puts YZY firmly in the watchlist category for traders looking for event‑driven volatility.

BR – $5.69M unlock

BR stands out with an unlock of roughly $5.69M against a relatively modest market cap of $29.27M and a price of $0.117. Only 17.69% of supply is currently released, underscoring a distinctly early‑curve profile where each large unlock significantly changes circulating supply.

This combination of low Released % and high unlock‑to‑cap ratio makes BR one of the more fragile profiles of the week from a dilution standpoint, and traders will be attentive to whether unlocked tokens are likely to be held, staked, or sold into secondary markets.

SEI – $3.90M unlock

SEI has an upcoming unlock of about $3.90M, with a reported market cap of $371.86M and a price of $0.055. With 59.77% of supply released, SEI is also in a mid‑curve emission stage where recurring unlocks continue to expand circulating float but are less extreme than early‑stage cliffs.

The unlock is material but not dominant relative to SEI’s market cap, suggesting that while localized volatility is likely, systemic spillover is less probable unless compounded by adverse macro or project‑specific news.

UDS – $2.52M unlock

UDS is scheduled to unlock approximately $2.52M in tokens, with a reported market cap of $186.78M and a price of $1.17. With 76.48% of its supply released, UDS sits in a late‑mid to mature curve, where new emissions are still relevant but occur against a larger circulating base.

The unlock is notable in nominal terms but likely represents a modest single‑digit percentage of market cap, suggesting manageable dilution under normal liquidity and demand conditions.

ZK – $1.95M unlock

ZK will unlock approximately $1.95M in tokens, versus a $114.34M market cap and a price of $0.012. With only 30.23% of supply released, ZK remains in an early emission phase where each unlock continues to materially expand circulating float.

While smaller than the very top‑tier events, the combination of early‑curve status and non‑trivial unlock size makes ZK relevant for participants focused on emerging infrastructure and zero‑knowledge‑aligned narratives.

Mid‑tier and micro unlocks

Mid‑tier unlocks ($50K–$1M range)

A cluster of projects falls into a mid‑tier bracket where unlocks are large enough to drive asset‑specific volatility, especially for tokens with moderate liquidity and active communities. Key examples include:

- SOLV – $629.23K unlock on a $5.08M market cap with 42.82% released; early‑mid curve with a relatively high unlock‑to‑cap ratio for a smaller asset.

- PIXEL – $494.27K unlock on a $4.33M market cap with 56.56% released; mid‑curve project where weekly emissions can still move the needle.

- BMT – $256.13K unlock on a $3.38M market cap with 65.11% released.

- ZKJ – $208.72K unlock on a $4.09M market cap with 53.18% released.

- GAL – $212.71K unlock on a $35.86M market cap with 90.34% released; late‑curve token where emissions are more incremental.

- DMC – $190.47K unlock on a $3.39M market cap with 53.89% released.

- LISTA – $82.66K unlock on a $20.41M market cap with 59.47% released.

- SVL – $91.34K unlock on a $12.90M market cap with 87.80% released.

Additional mid‑tier unlocks in the tens of thousands of dollars from ASTR ($57.44K), HOOK ($51.00K), FLIX ($30.61K), NAVX ($19.75K), NYAN ($8.86K), MMX ($12.19K), and YALA ($3.53K) can still create sharp intraday moves in thinner markets but are unlikely on their own to drive cross‑market sentiment.

Micro unlocks (<$100K, low absolute size)

At the bottom of the distribution are micro unlocks with very small scheduled values:

- FORT – $638.55 unlock on an $8.39M market cap with 61.57% released.

- SLF – $564.32 unlock on a $62.00K market cap with 71.59% released.

- VOXEL – $2.38K unlock on a $986.41K market cap with 85.92% released.

These events have limited systemic impact but can still be relevant for niche traders and small‑cap specialists, particularly where circulating supply is small and order books are extremely thin.

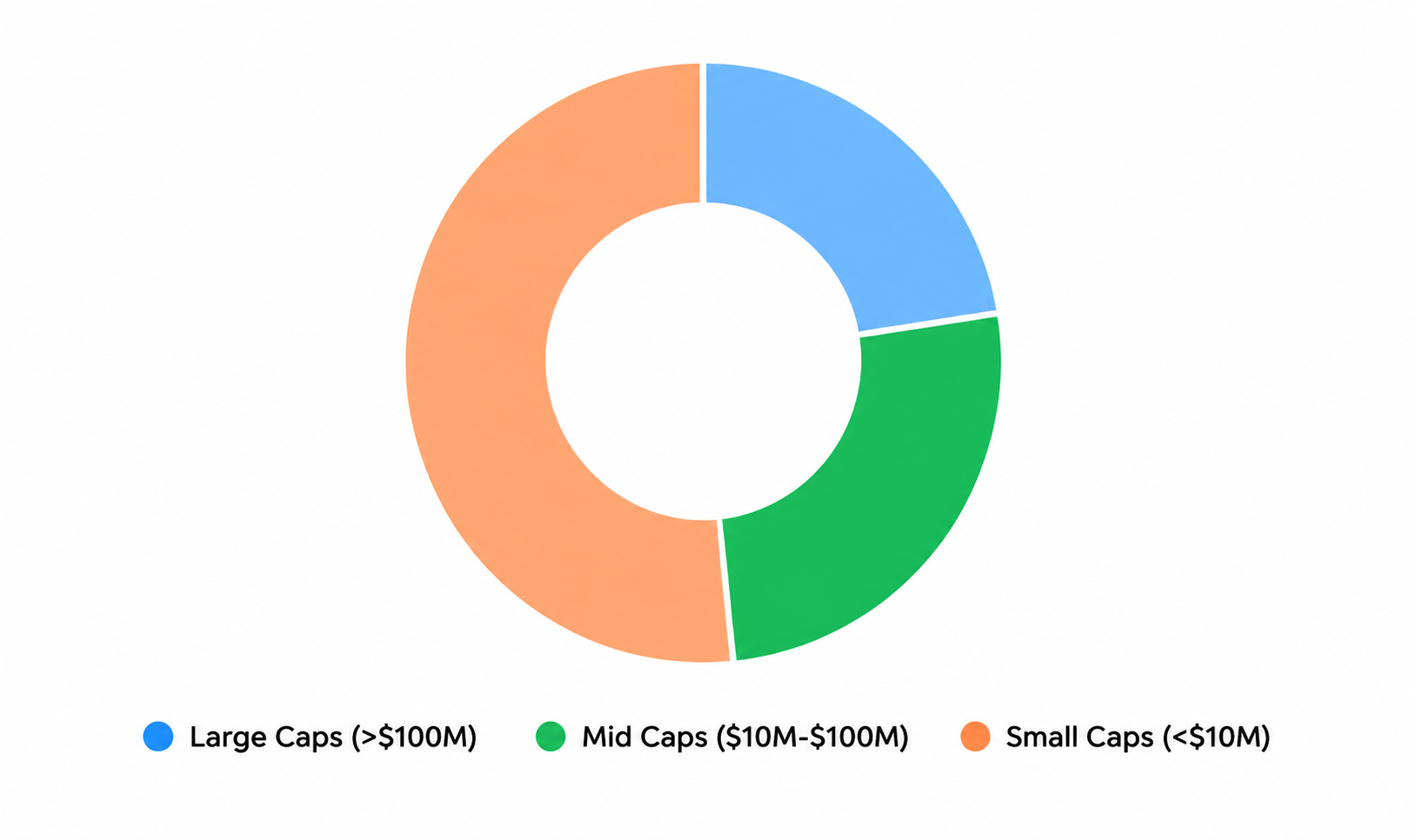

Market cap segmentation

This week’s token unlocks span large-cap, mid-cap, and micro-cap projects, creating varying levels of supply pressure across the market. While larger-cap assets typically absorb new supply more efficiently, smaller-cap tokens remain more vulnerable to volatility as unlocks can represent a significant share of circulating liquidity.

Market Cap Segmentation

Market Cap Segmentation

Large and near‑large caps

ARB ($536.43M), SEI ($371.86M), AERO ($359.69M), ZRO ($241.47M), UDS ($186.78M), and ZK/KAITO (both around $114M market caps) sit near the top of this week’s market‑cap range. For these tokens, unlocks often represent low‑ to mid‑single‑digit percentages of market cap, which are usually absorbed more smoothly thanks to deeper liquidity and broader holder bases.

Even so, large nominal events such as ZRO’s $23.16M or SPK’s $18.49M (despite its smaller cap) will be watched as sentiment drivers for infrastructure‑style and ecosystem projects.

Mid caps (roughly $10M–$200M)

This band includes:

- Upper mid to large: ZRO, KAITO, ZK, UDS, and other infra‑style names just below the largest‑cap cohort.

- Lower to standard mid caps: BR ($29.27M), YZY ($38.62M), GAL ($35.86M), KAT ($13.53M), ID ($12.21M), SOLV ($5.08M), BMT ($3.38M), DMC ($3.39M), NAVX ($5.70M).

In this group, unlocks from hundreds of thousands to several millions of dollars can equate to multiple percentage points of market cap in new supply, making weekly emissions a critical input for short‑term price action and risk management.

Small and micro caps (<$10M)

Tokens such as NAVX ($5.70M), SOLV ($5.08M), BMT ($3.38M), DMC ($3.39M), PIXEL ($4.33M), MMX ($1.26M), HOOK ($1.85M), VOXEL ($986.41K), NYAN ($172.32K), SLF ($62.00K), and YALA ($93.11K) sit at the bottom end of the size spectrum. In this cohort, even relatively small absolute unlocks can represent double‑digit percentages of effective float or traded liquidity, amplifying price sensitivity to event‑driven flows and order book imbalances.

Supply curve and sector‑level observations

The “Released %” column offers a clear view of where each token sits in its emission curve.

Early curve (≈40% or less released)

Early‑curve projects in this calendar include:

- BR (17.69%), YALA (26.71%), NYAN (28.58%).

- ZK (30.23%), SPK (33.01%), KAT (27.08%).

These tokens typically face recurring structural dilution and more event‑like unlocks, where each week’s schedule can materially change float and inform short‑term trading theses.

Mid curve (≈40–70% released)

Mid‑curve names include:

- SOLV (42.82%), CATI (47.50%), YZY (48.75%), ZKJ (53.18%), ARB (55.21%), ASTR (55.96%), PIXEL (56.56%), SEI (59.77%), LISTA (59.47%), FORT (61.57%), AERO (62.05%), BMT (65.11%), ID (72.06 – upper mid).

In this band, unlocks remain important drivers of weekly float changes but occur against a growing circulating base, making the impact more nuanced and dependent on market conditions.

Late curve (≈70–80%+ released)

Late‑curve projects (more than ~70–80% released) include:

- SLF (71.59%), VOXEL (85.92%), UDS (76.48%), HOOK (73.67%).

- GAL (90.34%), SVL (87.80%), NAVX (87.92%).

For these tokens, emissions are increasingly incremental relative to total supply, and unlocks tend to be more predictable, although they can still influence short‑term order flow and funding dynamics.

Sector‑wise, the mix spans:

- Infrastructure and DeFi‑aligned tokens such as ARB, SEI, AERO, ZRO, ZK, KAITO, UDS.

- Ecosystem, gaming, and community‑leaning tokens such as PIXEL, VOXEL, BR, NYAN, YZY, HOOK, NAVX, SVL.

Market impact assessment

Price pressure considerations

Relative unlock size and emission stage remain the two key determinants of potential price pressure, alongside the specifics of vesting schedules. Tokens where weekly unlocks likely exceed high single‑digit percentages of market cap and with low Released % (early‑curve names) are the most likely candidates for meaningful post‑unlock volatility.

Notable higher‑risk profiles in this week’s schedule include:

- SPK – $18.49M unlock vs $56.04M cap with 33.01% released; early‑mid curve with high unlock‑to‑cap ratio.

- BR – $5.69M unlock vs $29.27M cap with 17.69% released; early curve, structurally dilutive.

- YZY – $6.23M unlock vs $38.62M cap with 48.75% released.

- ZK – $1.95M unlock vs $114.34M cap with 30.23% released; early‑curve infra‑style token.

- SOLV, PIXEL, BMT, DMC – mid‑cap and small‑cap unlocks where six‑figure events are meaningful versus market cap and liquidity.

These tokens are most vulnerable to post‑unlock selling pressure, particularly if recipients are early investors, team wallets, or ecosystem funds with incentives to rebalance or realize gains.

Liquidity absorption capacity

The $86.21M weekly total tracked in this sheet is modest compared to the largest prior weeks but is heavily skewed toward a handful of names, making their ability to absorb new supply critical to how the market interprets the calendar. For mid caps and small caps, order-book depth, venue coverage, the distribution of unlocked tokens (team vs community vs investors), and existing Vesting and Lockups arrangements will dictate whether events are absorbed smoothly or lead to heightened volatility.

Strategic insights for investors and traders

During weeks with concentrated unlocks, investors and traders may consider monitoring tokenomics vesting updates alongside sentiment and liquidity. Understanding how much supply remains locked, the pace of future releases, and the percentage of tokens already in circulation can help market participants better assess dilution risks and potential event‑driven opportunities.

Key tactical considerations include:

- Position sizing and leverage control: Avoid heavy leverage or oversized positions in tokens facing unlocks that likely represent high single‑digit or greater percentages of market cap, especially early‑curve names with Released % under 40%.

- Event‑driven timing: Historical patterns often show selling into unlocks followed by relief once supply is digested; waiting for post‑event stabilization can reduce adverse entry points.

- Diversification across emission stages: Balance exposure between early, mid, and late‑curve tokens, prioritizing high Released % names (GAL, SVL, NAVX, VOXEL, UDS) when seeking reduced structural dilution.

Unlock weeks can also create constructive entry points, not just risk. Mature tokenomics names with more than 70–80% released supply face diminishing dilution after each event, so post‑unlock dips may offer medium‑term value, while high‑quality infrastructure names such as ARB, SEI, ZRO, and KAITO can offer long‑term accumulation opportunities if fundamentals remain strong.

Tokens to monitor closely

Based on absolute unlock size, unlock‑to‑market‑cap ratio, and emission stage, the following tokens warrant particular attention this week:

- ZRO – largest single unlock ($23.16M) on a $241.47M cap with 53.28% released; mid‑curve flagship event.

- SPK – $18.49M unlock vs $56.04M cap with 33.01% released; early‑mid curve, high ratio, clear overhang.

- KAITO – $7.40M unlock vs $114.35M cap with 39.19% released; mid‑curve infra‑style token.

- ARB – $8.04M unlock vs $536.43M cap with 55.21% released; larger‑cap infra anchor.

- SEI – $3.90M unlock vs $371.86M cap with 59.77% released; mid‑curve L1/L2‑style asset.

- BR – $5.69M unlock vs $29.27M cap with 17.69% released; early‑curve, structurally dilutive.

- YZY – $6.23M unlock vs $38.62M cap with 48.75% released; mid‑curve, strong unlock‑to‑cap ratio.

- ZK – $1.95M unlock vs $114.34M cap with 30.23% released; early‑curve infra category.

The week of June 15–21, 2026 therefore presents a focused $86.21M token unlock calendar across 31 projects, led by ZRO, SPK, KAITO, ARB, SEI, BR, UDS, YZY, and ZK and reinforced by mid‑tier and micro‑cap unlocks. For the broader market, these events are largely project‑specific and anticipated, but for individual tokens especially those with early‑curve tokenomics and large relative unlocks, short‑term price risk is elevated, creating both challenges and event‑driven opportunities for prepared participants.

You May Also Like

Robotics Automation Prototyping: Engineering Kinetic Agility into End-Effectors

Craving work-life balance is a huge red flag, says Fortune 500 Europe CEO—and like Barack Obama, he happily works through weekends

China Nabs Another Huione Group Core Member in Cambodia Extradition