Diagnosed With a Serious Illness at 62, Why He Claims His $2,300 Social Security Check Now Instead of Waiting for 70

The post Diagnosed With a Serious Illness at 62, Why He Claims His $2,300 Social Security Check Now Instead of Waiting for 70 appeared first on 24/7 Wall St..

- Claiming Social Security at 62 provides roughly $27,600 yearly income, covering a significant portion of a $78,535 annual budget without depleting savings for medical expenses.

- If health issues suggest you won't reach early 80s break-even age, claiming at 62 is prudent because total collected benefits matter more than individual payment amounts.

- Are you ahead, or behind on retirement? SmartAsset's free tool can match you with a financial advisor in minutes to help you answer that today. Each advisor has been carefully vetted, and must act in your best interests. Don't waste another minute; learn more here.

When a Diagnosis Rewrites the Retirement Plan

He spent years planning to wait until 70 for the biggest possible monthly check. Then a doctor’s diagnosis shortened his life expectancy, and the spreadsheet stopped making sense overnight.

He is 62, single, and eligible for roughly $2,300 a month if he claims now. The question becomes how to get the most out of the years he actually has, rather than how to maximize a lifetime of checks. On retirement forums, versions of this scenario appear often: someone who planned to delay, a sudden health event, and a frantic attempt to rework decades of assumptions in weeks.

This is one of the few moments where the conventional advice quietly flips. As Suze Orman put it on her May 4, 2025 podcast episode Suze School: The Actions You Need To Take Now, With Your Money: “Now obviously there are situations where taking it at 62 may make sense. You’re ill, you have a terminal illness… there are situations.”

The Break-Even Age Is the Whole Ballgame

Social Security lowers your monthly check for every year you claim before full retirement age (FRA), and pays you more for every year you wait past it, up to age 70. Claiming at 62 instead of FRA can cut the monthly benefit by up to roughly 30%. Delaying past full retirement age adds about 8% per year until 70.

That sounds like a clear case for waiting, but only if you live long enough to collect the difference. The break-even age, where total lifetime benefits from delaying surpass total benefits from claiming early, typically falls in the early 80s. Live past it, and waiting wins. Pass away before it, and every year of delay was a year of checks you never cashed.

With his numbers: at $2,300 a month starting at 62, he collects about $27,600 a year. If he waited to 70, the check would be considerably larger, but he would skip eight years of payments worth somewhere north of $220,000 in foregone income. For a healthy 62-year-old, that gap eventually closes. For someone whose doctors are talking in shorter time horizons, it may never close at all.

That is the entire decision: the number of checks matters more than the size of each one.

How the Rest of the Picture Shifts

Claiming early also changes how he uses everything else. Every dollar Social Security covers is a dollar he does not have to pull from savings, which means more cash stays liquid for things like medical costs, travel, or family needs. For a typical older household, average annual expenditures run around $78,535, so $2,300 a month covers a meaningful slice of the budget without touching the brokerage account.

Taxes deserve attention too. Once Social Security stacks on top of withdrawals from a traditional IRA or 401(k), up to 85% of the benefit can become taxable. Because he is single, the thresholds hit faster than for a married couple, so coordinating withdrawals with the new Social Security income matters more.

One reason this decision is cleaner for him than for many: he is single. A married higher earner must weigh that claiming early permanently shrinks the survivor benefit a spouse would inherit. Without a spouse depending on his record, that pressure disappears.

What to Sit With Before Filing

The hardest mistake to undo here is the opposite of what most advice columns warn about. The usual worry is claiming too early and regretting the smaller check at 85. In his case, the regret would be waiting for a bigger check that never arrives.

A few things worth doing before he files:

- Pull a personalized benefit estimate from Social Security directly so the $2,300 figure reflects his actual earnings record, not a rough sketch.

- Map out which accounts he would otherwise tap first, and whether starting Social Security now lets tax-deferred balances keep growing or pass to heirs more efficiently.

- Revisit the decision if his prognosis improves. Claiming is not entirely irreversible in the first 12 months, and circumstances change.

Prognoses are estimates, not verdicts, and some people outlive them by years. Early claiming is not the right call for everyone facing a serious diagnosis, but the standard “wait until 70” advice quietly assumes a long life, and when that assumption breaks, the math should break with it.

If You’ve Been Thinking About Retirement, Pay Attention (sponsor)

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance, and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor. Here’s how:

-

Answer a Few Simple Questions.

-

Get Matched with Vetted Advisors

-

Choose Your Fit

Why wait? Start building the retirement you’ve always dreamed of. Get started today! (sponsor)

The post Diagnosed With a Serious Illness at 62, Why He Claims His $2,300 Social Security Check Now Instead of Waiting for 70 appeared first on 24/7 Wall St..

You May Also Like

Q2 Market Insights: Bitcoin regains dominance in risk-averse environment, ETFs remain critical to market structure

Hedera Price Prediction Holds Bullish as Iran Peace Deal Pushes Bitcoin Above $65,000 and Pepeto Presale Passes $10 Million

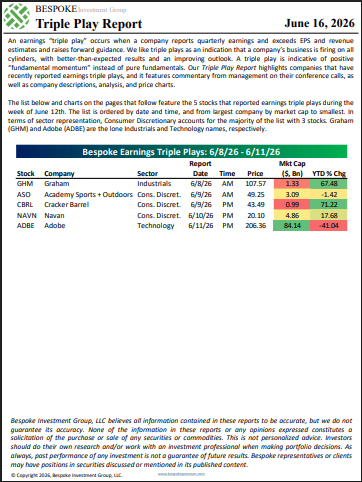

The Triple Play Report: 6/16/26