Plug Power Lost 97% of Its Value Over Five Years. The Margin Turnaround in 2026 Is Why Analysts Are Starting to Look Again

Key Stats for Plug Power Stock

- 52-Week Range: $1.09 to $4.58

- Current Price: $2.71

- Street Mean Target: $3.62

- Market Cap: $3.78B

- Q1 2026 Revenue: $163.5M (+22% YoY)

- Q1 2026 Gross Margin: -13% (vs. -55% prior year)

- Q1 2026 Adjusted EPS: -$0.08 (vs. -$0.17 prior year)

- Total Cash Including Restricted: ~$802M

Value your favorite stocks like PLUG with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

The DOE Loan Closed, the Margins Started Moving, and the Going-Concern Story Finally Changed

Plug Power (PLUG) spent most of 2025 convincing investors it would survive. The question now is whether the ongoing margin recovery is fast enough to justify the stock’s $2.71 price.

The company was in genuine trouble two years ago. Revenue fell from $891 million in 2023 to $629 million in 2024 as hydrogen plant outages disrupted fuel deliveries and customers pulled back. Gross margins collapsed to negative 92% that year, meaning Plug was losing nearly a dollar for every dollar of revenue it brought in. The going-concern disclosure followed, the stock cratered, and the debate shifted from growth to survival.

Two things changed the narrative. The DOE closed a $1.66 billion loan guarantee, removing the risk of bankruptcy and funding the construction of six new green hydrogen production facilities. And then the operating metrics started moving in the right direction.

See analysts’ growth forecasts and price targets for PLUG stock (It’s free!) >>>

A 36% Drawdown From the 2026 High and a Stock Sitting at Its Worst Level of the Year

Plug Power peaked above $4 earlier this year as the DOE loan closed and contract wins came in, including a 275-MW electrolyzer deal with Hy2gen in Quebec.

The stock has since given back nearly everything, with a maximum drawdown of 36% recorded on June 17, and the current price is just above that low.

Plug Power Drawdowns. (TIKR)

Plug Power Drawdowns. (TIKR)

The selloff looks disconnected from the Q1 2026 results, which were the most encouraging the company has posted in years. Revenue came in at $163.5 million, up 22% year over year. Gross margin improved to negative 13% from negative 55% in the prior year period, a 71% improvement.

Adjusted EPS narrowed to negative $0.08 from negative $0.17. CEO Jose Luis Crespo said the quarter “positions us to achieve our EBITDAS positive target in Q4 2026.”

See analysts’ growth forecasts and price targets for Plug Power stock (It’s free!) >>>

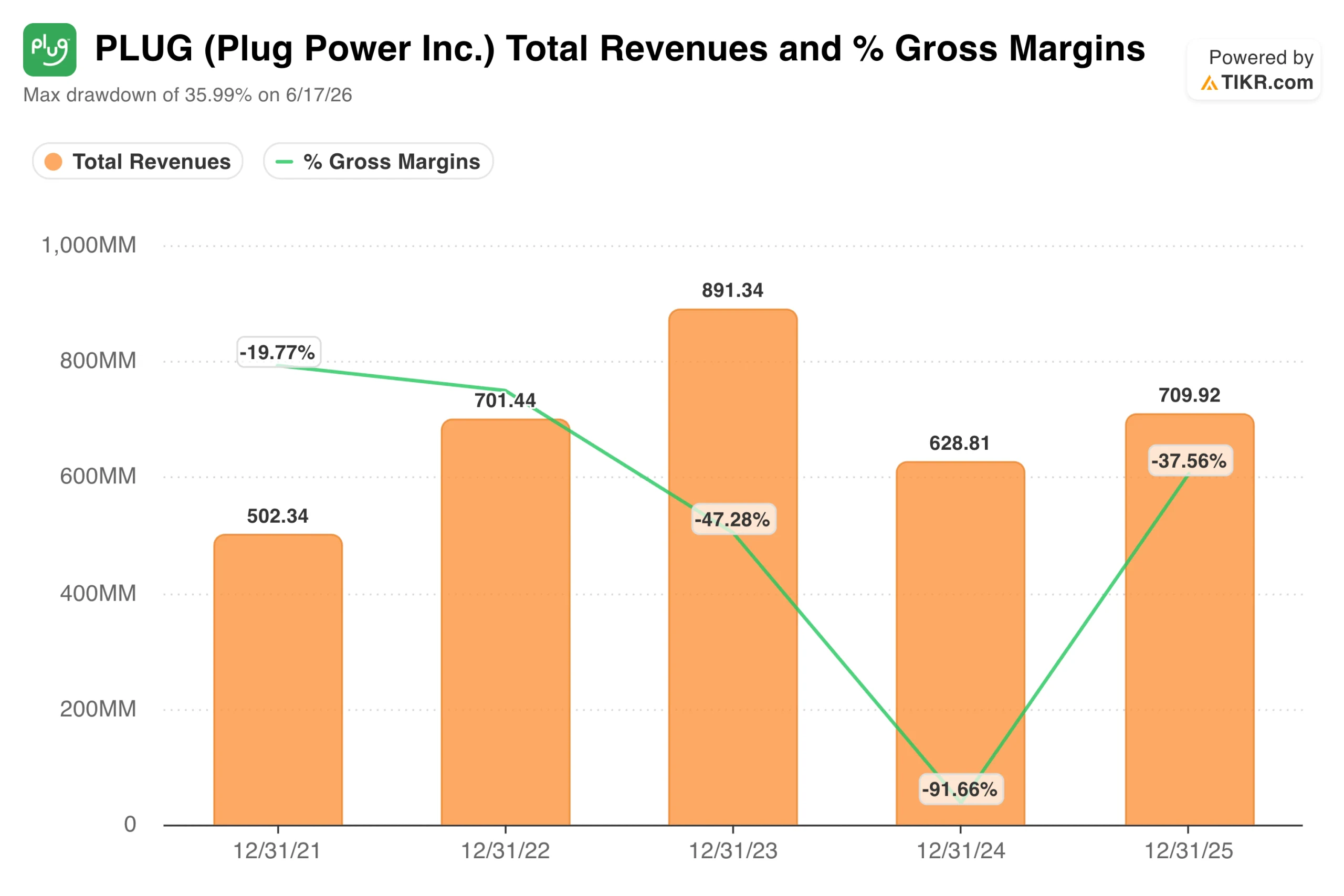

Revenue Back Above $700 Million, Gross Margins Off the Floor, and the 2024 Crater Starting to Look Like a Bottom

The revenue and gross margin chart tells the story of the last four years in one picture. Revenue grew from $502 million in 2021 to $891 million in 2023, then fell sharply to $629 million in 2024 as the business hit an operational wall. Gross margins trended worse the whole time, bottoming at-92% in 2024 before bouncing back to-38% in 2025.

Plug Power Total Revenues, Gross Margins. (TIKR)

Plug Power Total Revenues, Gross Margins. (TIKR)

Revenue recovered to $710 million in 2025, and the Q1 2026 trajectory suggests continued growth. The margin recovery matters more. Getting from negative 92% back toward zero is not a small thing, and the Q1 2026 gross margin of negative 13% suggests 2024 was genuinely the trough.

Plug now has over 74,000 GenDrive fuel cell systems operating across more than 280 material-handling sites. Walmart, Amazon, Home Depot, and BMW are among the customers. The electrolyzer business has deployed over 320 MW of capacity globally.

The path to profitability runs through two milestones: gross margin breakeven, which management expects in 2026, and EBITDAS positive, targeted for Q4 2026. Neither is guaranteed, and both require continued execution on cost reduction, hydrogen plant uptime, and service margin improvement.

Wall Street’s Take: A $3.62 Mean Target, a $7 Bull Case, and a $0.75 Bear Case

The Street Targets table captures how wide the range of outcomes is. The mean analyst target has risen from $1.85 a year ago to $3.62 today as the margin recovery is starting to show up in the numbers. The stock currently trades at a 33% discount to that mean.

Street Targets. (TIKR)

Street Targets. (TIKR)

The high target of $7.00 and the low of $0.75 are not just bookends. They reflect a genuine split on whether the Q4 2026 profitability target is achievable and whether Plug’s vertically integrated hydrogen model can compete at scale. There are currently 5 buys, 12 holds, and 3 sells among the 16 analysts covering the stock.

The bull case is that the margin recovery is real, the DOE loan eliminates capital risk, and data center demand for on-site hydrogen power gives Plug a tailwind it did not have two years ago. The bear case is that cash burn continues, dilution has been severe, gross margins are still deeply negative, and the EBITDAS target has been pushed back before.

Plug Power is not a stock for investors who want certainty. It is a stock for investors who think the 2024 margin collapse was a cyclical low rather than a structural one, and that the company now has enough capital and commercial momentum to prove it.

Value Plug Power instantly (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

House Democrats Question SEC on AI Agent Advisor Oversight

Ozak AI 888 Fortune Campaign Live: Ecosystem Prepares For Launch

China Nabs Another Huione Group Core Member in Cambodia Extradition