Micron Hits New Highs, Here’s What Smart Investors Are Doing

The post Micron Hits New Highs, Here’s What Smart Investors Are Doing appeared first on 24/7 Wall St..

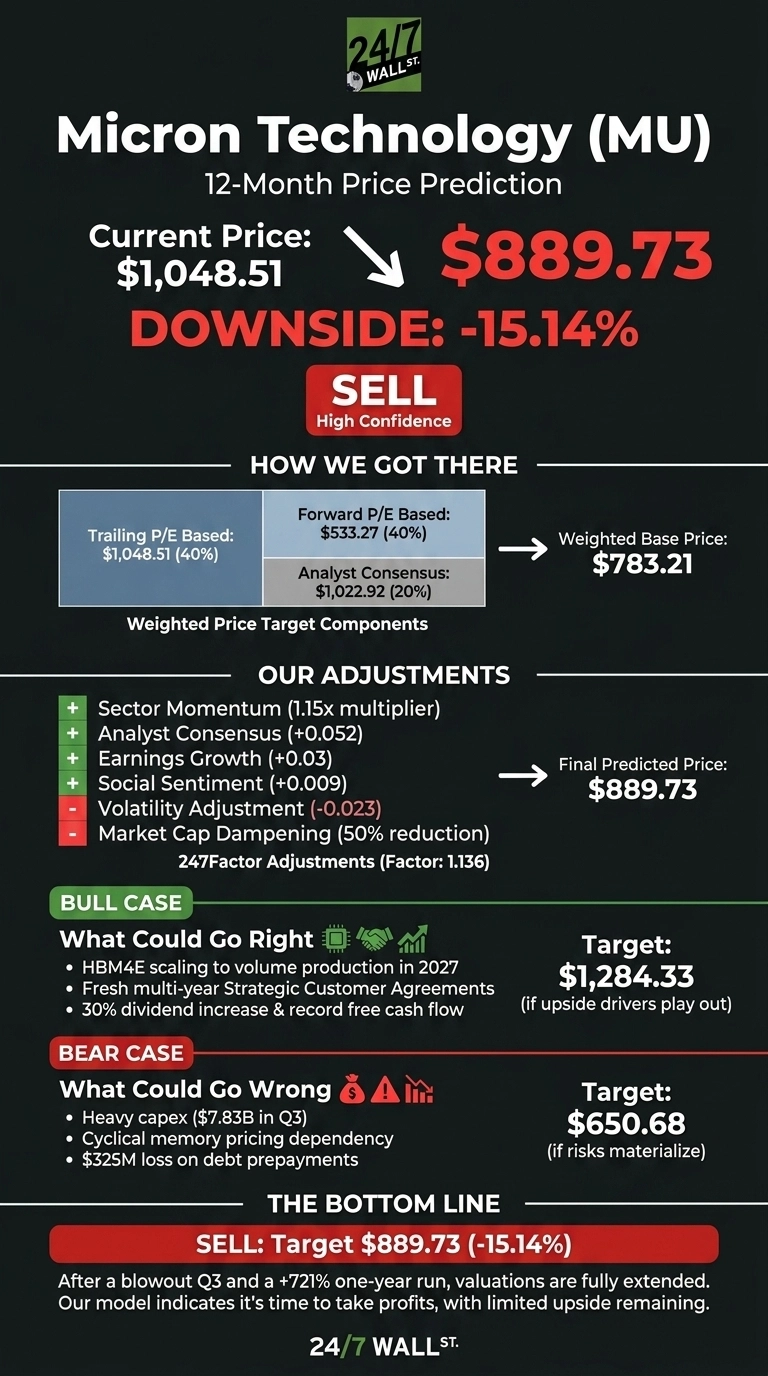

Micron Technology (NASDAQ:MU) has climbed from roughly $127.60 a year ago to past $1,048 as the AI memory cycle accelerated. After a blowout fiscal Q3, our proprietary model says the easy money has already been made.

Our 24/7 Wall St. price target for Micron is $889.73, implying 15.14% downside from the current $1,048.51 level. We rate shares a sell with high confidence (90%). The trailing valuation is fully extended, insider selling has been unusually heavy at peak prices, and the forward setup leaves limited room for a positive surprise.

24/7 Wall St.

24/7 Wall St.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $1,048.51 |

| 24/7 Wall St. Price Target | $889.73 |

| Upside/Downside | -15.14% |

| Recommendation | SELL |

| Confidence Level | 90% |

A Note Before We Begin

Our 24/7 Wall St. price target of $889.73 sits below where Micron trades today. Real upside could come from HBM4E scaling to volume production in calendar 2027 or fresh multi-year Strategic Customer Agreements extending revenue visibility well past fiscal 2027. Consider our target one datapoint among many. A detailed bull case appears below.

A Historic Run Built on a Blowout Quarter

Micron’s price action has been extraordinary. Shares are up 267.54% YTD, 721.72% over one year, and 39.62% in the past month.

The trigger was Q3 FY2026 earnings released June 24: revenue of $41.46B versus $35.25B consensus, a 17.60% beat and +345.7% YoY, with non-GAAP EPS of $25.11 versus $20.28 expected. GAAP gross margin hit 84.6%, a 46.9 point YoY expansion.

CEO Sanjay Mehrotra called the results evidence of “the strategic value of memory in the AI era.” Q4 guidance of $50B in revenue and $31 EPS at the midpoint suggests momentum continues. Shares now sit just 16% below the 52-week high of $1,213.56.

Why Bulls See a Breakout Ahead

Bulls have ammunition. 39 of 44 analysts rate MU a buy, with a consensus target of $1,022.92. HBM4 is already in high-volume shipments to the lead customer, and HBM4E volume production is teed up for 2027. Free cash flow hit $18.30B in Q3 alone, up 995% YoY, and management approved a 30% dividend increase.

If Q4 lands at the $31.00 EPS guide, the forward multiple compresses fast. Our bull scenario tags MU at $1,284.33 over 12 months, a 22.49% return, with a path to $1,305.77 by May 2027.

Several analysts expect a strong upside. Barclays analyst Tom O’Malley raised the firm’s price target on Micron to $2,000 from $1,175 and keeps an Overweight rating following the earnings report while BofA raised the firm’s price target to $1,550 from $1,500 and keeps a Buy rating. Citi raised the target to $1,400 with a Buy rating and Goldman Sachs raised the target to $1,100 with a Neutral rating.

The Risks Worth Watching

Insider activity is the loudest warning. CEO Mehrotra sold across 63 separate transactions on May 1 and May 29, with May 29 prints between $942.14 and $979.37. Capex ran $7.83B in Q3, and a $325M loss on debt prepayments hit the quarter.

Memory remains cyclical, HBM4 carries lead-customer concentration risk, and Reddit’s WSB sentiment registers 40 versus 88 in options threads, signaling fraying conviction at the edges.

Bulls would argue insider selling reflects portfolio diversification at all-time highs rather than a fundamentals call, and that record capex locks in HBM share through 2027. Our bear case implies $650.68 over 12 months, a 37.94% drawdown.

The Risk Isn’t Worth the Reward Here

The 24/7 Wall St. price target of $889.73, a sell rating, and 90% confidence reflect a stock that has priced in two years of perfect execution inside six months. We would be a buyer below $750, where forward P/E sinks toward 13x.

We would stay sidelined above $1,000 until Q4 actuals confirm the $31 EPS guide and Strategic Customer Agreement detail emerges. After a +538% move since September 2025, the setup favors patience over chasing.

Micron Price Prediction 2026-2030

Here is where our model projects Micron could trade as the AI memory cycle matures and pricing normalizes from current peaks.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $889.73 |

| 2027 | $870.00 |

| 2028 | $855.00 |

| 2029 | $842.00 |

| 2030 | $832.75 |

These projections assume Micron executes on HBM4 and HBM4E ramps while memory pricing mean reverts. Significant upside could come from a longer-than-expected AI capex cycle; meaningful downside could come from a hyperscaler digestion phase or a HBM share-loss event.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Micron Technology didn’t make the cut. Grab the names FREE today.

The post Micron Hits New Highs, Here’s What Smart Investors Are Doing appeared first on 24/7 Wall St..

You May Also Like

El Salvador’s Bitcoin reserve faces an accounting reckoning under new IMF pressure

Zcash Co-Founder Josh Swihart Unveils Roadmap to Eliminate Centralization Barriers

Bitget Unveils AI Agent Accounts to Enable Autonomous Crypto Trading