Generac Is Up 109% This Year. The Data Center Backlog Explains Why

Key Stats for Generac Stock

- 52-Week Range: $134.80 to $296.44

- Current Price: $280.66

- Street Mean Target: $284.00

- Market Cap: ~$17.4B

- LTM Gross Margin: 38.1%

- LTM EBIT Margin: 7.5%

- Forward 2-Yr Revenue CAGR: ~16%

- Forward 2-Yr EPS CAGR: ~33%

- NTM P/E: ~32x

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

C&I Revenue Jumped 28% as Data Centers Take Over

Most investors know Generac (GNRC) as the company that sells home standby generators during hurricane season. That framing is increasingly outdated. The business that is driving the stock today is commercial and industrial power, specifically large-megawatt backup generators for data centers that cannot afford a single minute of downtime.

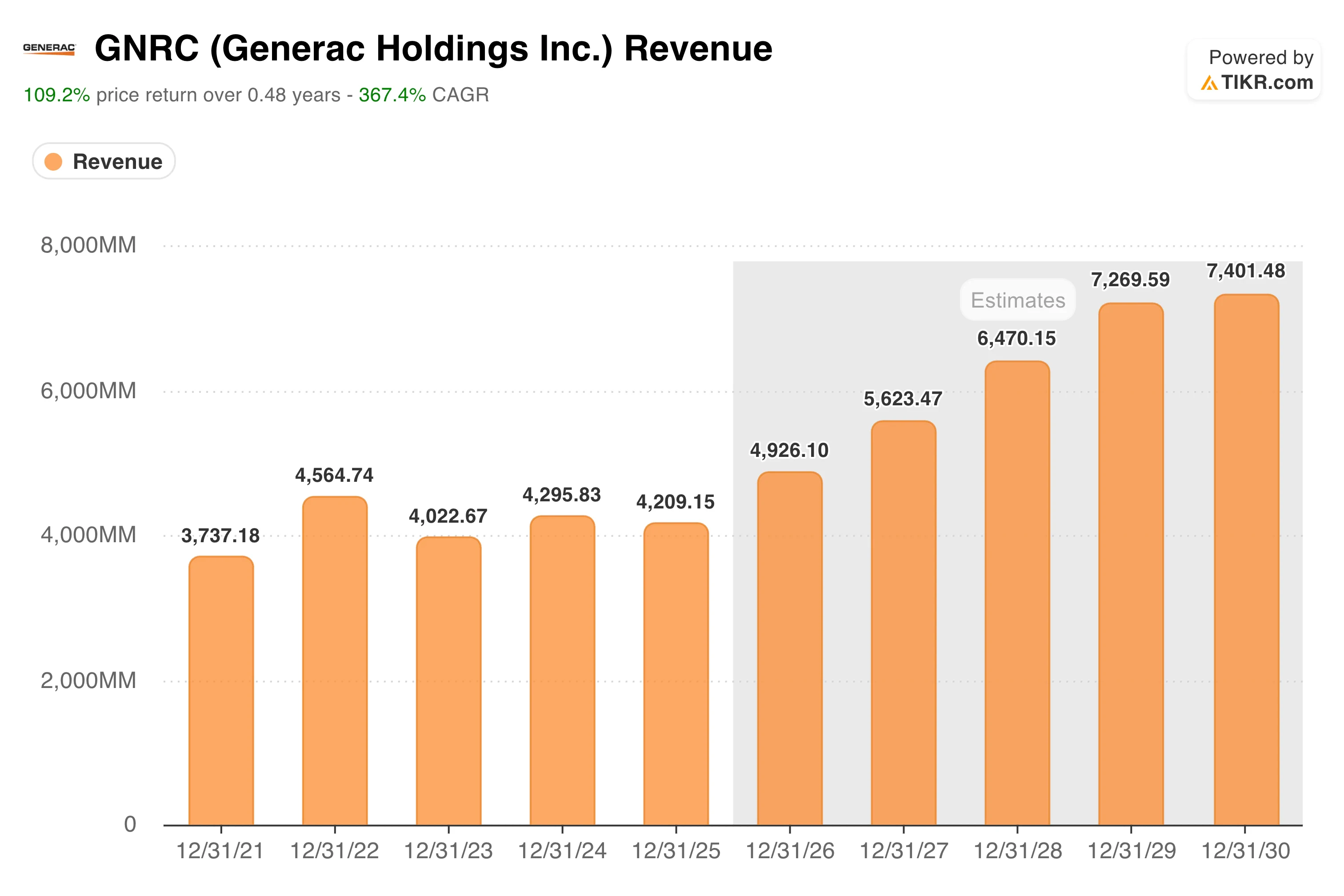

Revenue peaked at $4.56 billion in 2022 during the post-hurricane generator boom, then declined for two consecutive years as the residential cycle cooled sharply.

What has changed the trajectory is data center demand. In Q1 2026, the commercial and industrial segment grew 28% to $510 million, while the residential segment was essentially flat at $549 million. The two segments are now roughly equal in size, a mix shift that would have seemed implausible three years ago.

Generac Revenue Estimates. (TIKR)

Generac Revenue Estimates. (TIKR)

The backlog data tells the most compelling part of the story. CEO Aaron Jagdfeld reported that the data center backlog grew to more than $700 million by the Q1 earnings call, up roughly $300 million in just ten weeks since the prior update.

In June, Generac signed a formal global supply agreement with an undisclosed hyperscale data center operator, awarded after a rigorous qualification process that included multiple factory visits and audits across Generac’s supplier network.

A separate nonbinding notice to proceed with a second hyperscale customer represents approximately $600 million of potential 2027 deliveries not yet included in official guidance.

Management raised full-year 2026 guidance following Q1, now expecting mid-to-high teens revenue growth and adjusted EBITDA margins of 18.5 to 19.5%, up from the prior guidance range. Free cash flow more than tripled year over year to $90 million in the quarter alone.

See the exact moment Wall Street upgrades GNRC stock before the rest of the market piles in — track analyst rating changes in real time with TIKR for free →

The Stock Is at 19x EBITDA. History Puts That in Context.

Generac’s NTM EV/EBITDA multiple spent most of the decade prior to 2020 in the 10-13x range. It spiked above 30x during the pandemic generator frenzy of 2021, crashed back toward 8x as the residential cycle collapsed, and has now re-rated to around 19x on the back of the data center narrative.

Generac Holdings Total Enterprise Value. (TIKR)

Generac Holdings Total Enterprise Value. (TIKR)

That 19x multiple is well above the historical baseline but far below the 2021 peak. Whether it is justified depends on how much of the data center opportunity actually converts to sustained earnings.

The residential energy technology segment, which includes solar storage and smart home products, remains below EBITDA breakeven and continues to absorb operating expenses. Getting onto a hyperscale operator’s approved vendor list is genuinely difficult and competitively significant, but delivering at scale against that backlog while managing margins is a separate challenge.

Generac competes against Caterpillar, Cummins, and Rolls-Royce in large-megawatt backup power, all of which have deeper industrial manufacturing infrastructure.

See what analysts think about GNRC stock right now (Free with TIKR) >>>

The Model Sees 20% Upside. The High Case Is More Interesting.

TIKR’s valuation model targets around $355 for Generac in the mid case, implying a total return of around 20% over roughly four and a half years, or about 4% annualized. That is a modest return relative to the risk involved, and it reflects a business where the Street has already priced in meaningful execution on the data center opportunity.

Generac Valuation Model. (TIKR)

Generac Valuation Model. (TIKR)

The more interesting scenario is the high case, which reaches around $530 and implies around 7% annualized returns. That requires roughly 7% revenue growth, net income margins expanding to around 13%, and continued multiple expansion as hyperscale agreements prove durable.

It is achievable, but it demands that Generac convert its backlog cleanly, ramp its new Wisconsin manufacturing facility on schedule, and defend its position against larger industrial competitors.

Should You Invest in Generac Holdings, Inc.?

Generac’s data center pivot is real, and the backlog is growing fast, but the stock has already doubled in six months and now trades above the street mean target.

The mid-case model implies only modest returns from here. Investors who believe the hyperscale opportunity is larger than consensus expects will find the high case compelling. Everyone else should wait for a better entry point.

See the full TIKR model for GNRC, including scenario assumptions and historical valuation multiples. Build your own valuation for Generac stock on TIKR for free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Bitcoin at Crucial Pivot Point, Here's Why Fed Can Tilt Balance

Russia's Lavrov Admits That Anchorage Only Bought Time For Ukraine To Rearm

Why Tokenized Stock STRCx Holds the Largest Market Cap in Its Class