Qualcomm Price Prediction: The Forecast Is Far More Bullish Than Analysts

The post Qualcomm Price Prediction: The Forecast Is Far More Bullish Than Analysts appeared first on 24/7 Wall St..

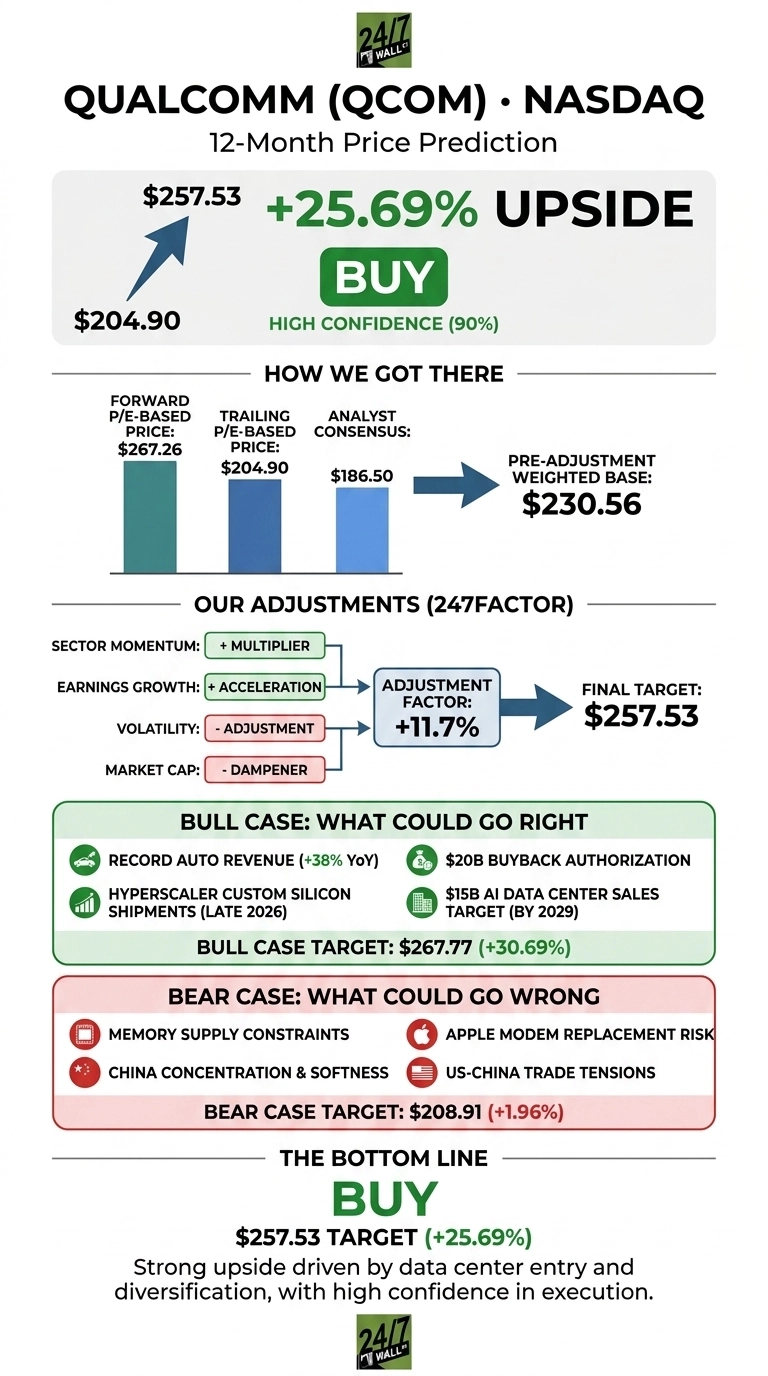

Our Qualcomm (NASDAQ:QCOM) price prediction sits well above where the sell side has landed, and that gap is the entire story. Wall Street’s consensus target of $186.50 implies downside from today’s quote.

Our model sees the opposite. The 24/7 Wall St. price target for Qualcomm is $257.53, pointing to roughly 25.69% upside over the next 12 months, with a 90% confidence read. The recommendation is buy.

24/7 Wall St.

24/7 Wall St.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $204.90 |

| 24/7 Wall St. Price Target | $257.53 |

| Upside | 25.69% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Sharp Pullback After an Even Sharper Rally

Qualcomm has had a wild quarter. The stock is up 21.03% year to date and 34.18% over the past year, but shares have given back 17.34% over the last month after touching $258.96 in May. The recovery off the March low near $129.39 followed a blowout Q1 FY26 earnings report and a Q2 report that delivered $2.65 non-GAAP EPS on $10.6 billion in revenue, a 3.67% EPS beat and the fourth consecutive quarter topping consensus.

The June 24 Investor Day was the catalyst behind this week’s bullish chatter. Management doubled the 2029 non-handset revenue target to $40 billion and laid out a $15 billion AI data center sales target, which triggered a +12% pre-market reaction. Retail sentiment on r/wallstreetbets jumped to 76 on the news.

The Case for $267 and Higher

The bull thesis rests on diversification finally cracking the “Qualcomm is just a handset story” narrative. Q2 FY26 automotive revenue hit a record $1.33 billion, up 38% YoY, while IoT grew 9%. CEO Cristiano Amon flagged that a “leading hyperscaler custom silicon engagement is on track for initial shipments later this calendar year,” validating the data center entry.

Add the Alphawave Semi acquisition, the Snapdragon AI-at-the-edge roadmap, a fresh $20 billion buyback authorization, and our bull case targets $267.77, a 30.69% total return.

The Risks Worth Watching

Q3 FY26 guidance of $9.2 billion to $10 billion in revenue and non-GAAP EPS of $2.10 to $2.30 implies another sequential decline. Handsets fell 13% YoY on memory supply constraints and China softness. Apple’s eventual modem in-sourcing, customer vertical integration, and US-China trade friction are real overhangs, and insider activity skews to net selling.

That said, management expects Chinese handset revenue to bottom in Q3 and recover sequentially. Bears would also note operating income dropped 26% YoY, though heavy data center R&D is a big reason why. Our bear case lands at $208.91.

Qualcomm Price Prediction 2026-2030

The 24/7 Wall St. price target of $257.53 reflects high confidence that the data center optionality is mispriced at a forward P/E of 18x. I’d be a buyer here if the hyperscaler shipments land on schedule in late 2026 and China handsets stabilize as guided.

I’d stay on the sidelines if Q3 guidance is cut again or if the Apple modem transition accelerates. The setup favors the bulls.

Looking further ahead, here is where our model projects QCOM could trade, assuming the data center ramp and FY29 revenue goals stay on track.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $257 |

| 2027 | $295 |

| 2028 | $335 |

| 2029 | $370 |

| 2030 | $400 |

These projections assume Qualcomm executes on its $40 billion non-handset 2029 target. Significant downside could result from Apple’s modem transition or a hyperscaler engagement slipping into 2027.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Qualcomm didn’t make the cut. Grab the names FREE today.

The post Qualcomm Price Prediction: The Forecast Is Far More Bullish Than Analysts appeared first on 24/7 Wall St..

You May Also Like

Bitcoin-Backed Lending Market Shifts Toward Institutional Players, SVB Report Finds

68% of global BTC miners came from the U.S., Russia, and China, Q1 2026