U.S. Dollar Powers Through Best Monthly Run Since Mid-2025 — And It May Not Be Over

Key Takeaways

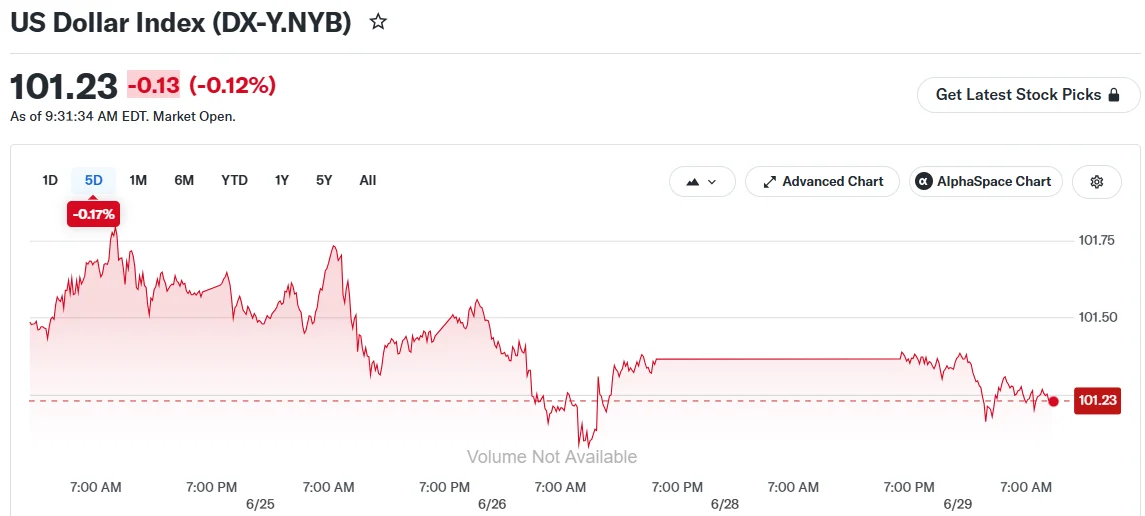

- U.S. Dollar Index dipped to 101.24 but continues trading near its highest level in 14 months

- The greenback is poised to record its strongest monthly advance since July 2025, climbing approximately 2.5% throughout June

- Diplomatic negotiations between Washington and Tehran are set to restart in Qatar, reducing risk-off currency flows

- Markets anticipate two additional Federal Reserve rate increases by year-end as inflation hovers above 4%

- This week’s focus centers on the ECB’s Sintra conference and critical U.S. employment figures

The greenback experienced a modest retreat on Monday while maintaining its position near a 14-month summit. Trading at 101.24 during morning U.S. sessions, the U.S. Dollar Index backed away from its June 24 high of 101.8.

US Dollar Index (DX-Y.NYB)

US Dollar Index (DX-Y.NYB)

The minor pullback hasn’t derailed what’s shaping up to be the currency’s most impressive monthly showing in nearly a year. June has delivered gains of roughly 2.5% for the index, marking the best single-month performance since July 2025.

Forces Behind the Dollar’s Rally

Multiple dynamics have sustained the dollar‘s upward trajectory. With inflation maintaining levels north of 4%, the Federal Reserve faces mounting pressure to adopt a more hawkish monetary policy approach. Financial markets have now priced in two additional quarter-point rate increases before 2025 concludes.

Robust economic indicators from the United States have reinforced this narrative. A durable jobs market has bolstered investor sentiment toward the currency, with this week’s non-farm payrolls data positioned as a critical barometer for future direction.

Investment flows into American artificial intelligence equities have provided additional support. International capital allocation toward Wall Street has maintained consistent underlying demand for assets denominated in dollars.

International Tensions and Monetary Policy Developments

The U.S.-Iran conflict had been a significant catalyst for safe-haven dollar positioning in preceding weeks. Following weekend military exchanges, both nations agreed to suspend hostile operations. Diplomatic discussions are scheduled to reconvene in Qatar on Tuesday.

The ceasefire has begun alleviating tension in worldwide energy markets. Crude oil valuations have started retreating toward pre-escalation benchmarks as shipping activity from the Persian Gulf normalizes following a memorandum of understanding between the two powers.

The euro gained 0.2% to reach $1.14 but continues trading near its lowest point in twelve months. Sterling maintained $1.32 as markets digested significant political developments. Following Keir Starmer’s resignation announcement last week, Andy Burnham has emerged as the leading candidate for succession.

The European Central Bank’s yearly Sintra gathering commences Monday. ECB President Christine Lagarde will deliver inaugural comments alongside Federal Reserve Chair Kevin Warsh and Bank of England Governor Andrew Bailey. Market participants anticipate at least one further ECB rate adjustment this year after the deposit facility rate reached 2.25%.

The yen showed minimal movement. Japan’s upcoming Bank of Japan Tankan survey is projected to reflect enhanced corporate confidence despite recent energy market volatility.

Throughout the Asia-Pacific region, market observers are monitoring China’s manufacturing indicators, South Korean export data, and India’s industrial output statistics for insights into regional central bank policy trajectories.

The dollar’s trajectory in coming days will hinge substantially on central bank rhetoric at the Sintra forum and Friday’s employment report findings.

The post U.S. Dollar Powers Through Best Monthly Run Since Mid-2025 — And It May Not Be Over appeared first on Blockonomi.

You May Also Like

Monday Market Wrap: Comcast Breakup, Alphabet’s Dow Debut, and Tech Stock Rally

Columnist cracks the 'unifying theory' behind Trump's seemingly manic behavior: opinion