Free Cash Flow of $1.7 Billion Puts Diamondback Energy Stock in Focus for Q2 2026

Key Takeaways for Diamondback Energy Stock as of June 2026

- Analysts rate Diamondback Energy stock 25 buys or outperforms, 4 holds, and 0 sells, with a mean target of $234, implying around 30% upside from the current price of $180.

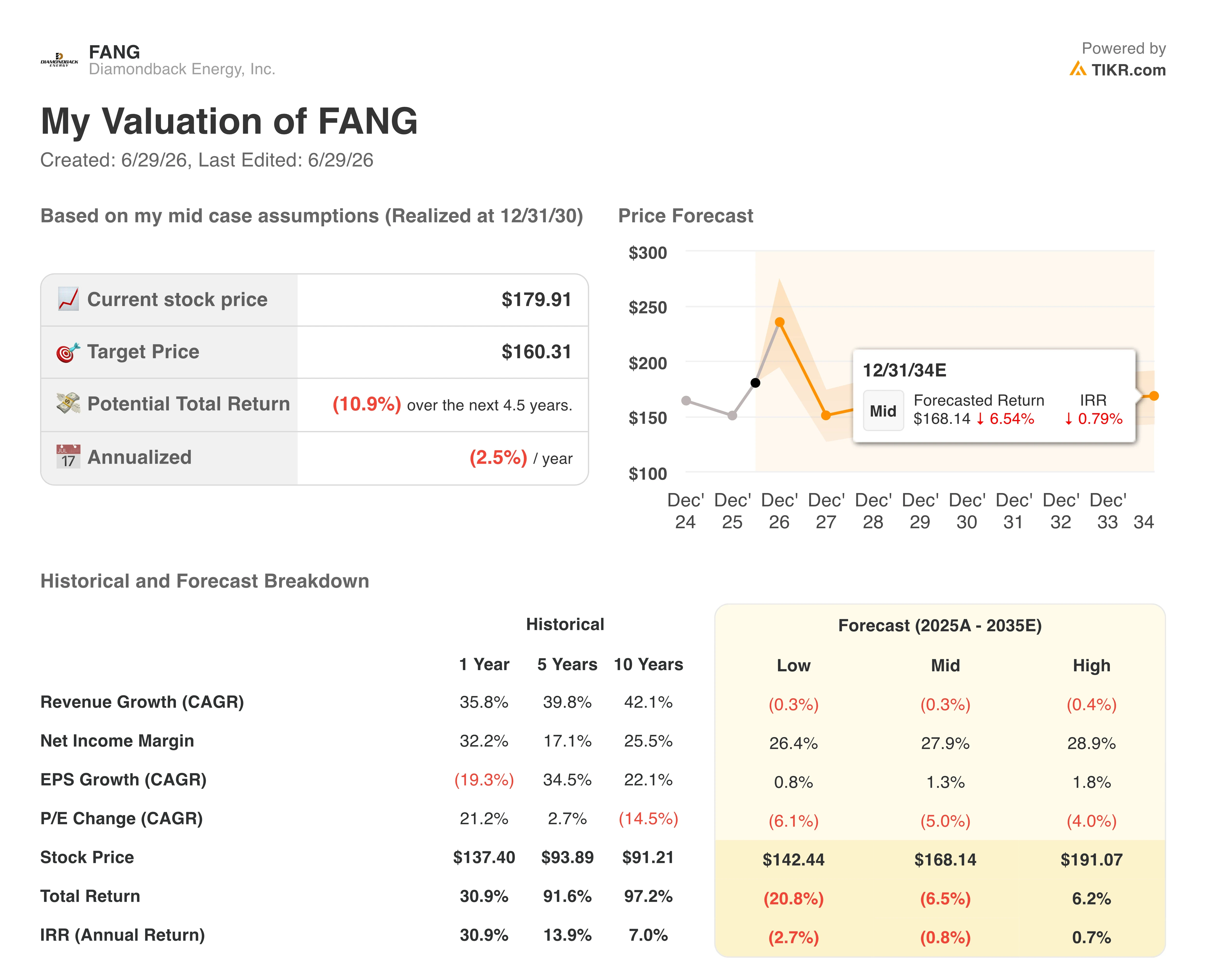

- TIKR’s mid-case model values Diamondback Energy at around $160 by December 2030, implying around 11% negative total return, or roughly 2.5% negative annualized over 4.5 years.

- Diamondback Energy stock appears overvalued at current levels, with Q1 free cash flow of $1.71 billion supported by oil prices the TIKR model does not assume persist at mid-cycle.

- Diamondback raised 2026 oil production guidance to above 520,000 barrels per day after Q1 output beat consensus, while the CFO outlined a path to $10 billion net debt within months.

Diamondback’s Street target sits 30% above the current price, while TIKR’s model points to 11% downside. See where the gap lives. Analyze FANG stock on TIKR for free →

Diamondback Energy Beats Q1 FCF by 9% but TIKR’s Model Says FANG Stock Is Overvalued at $180

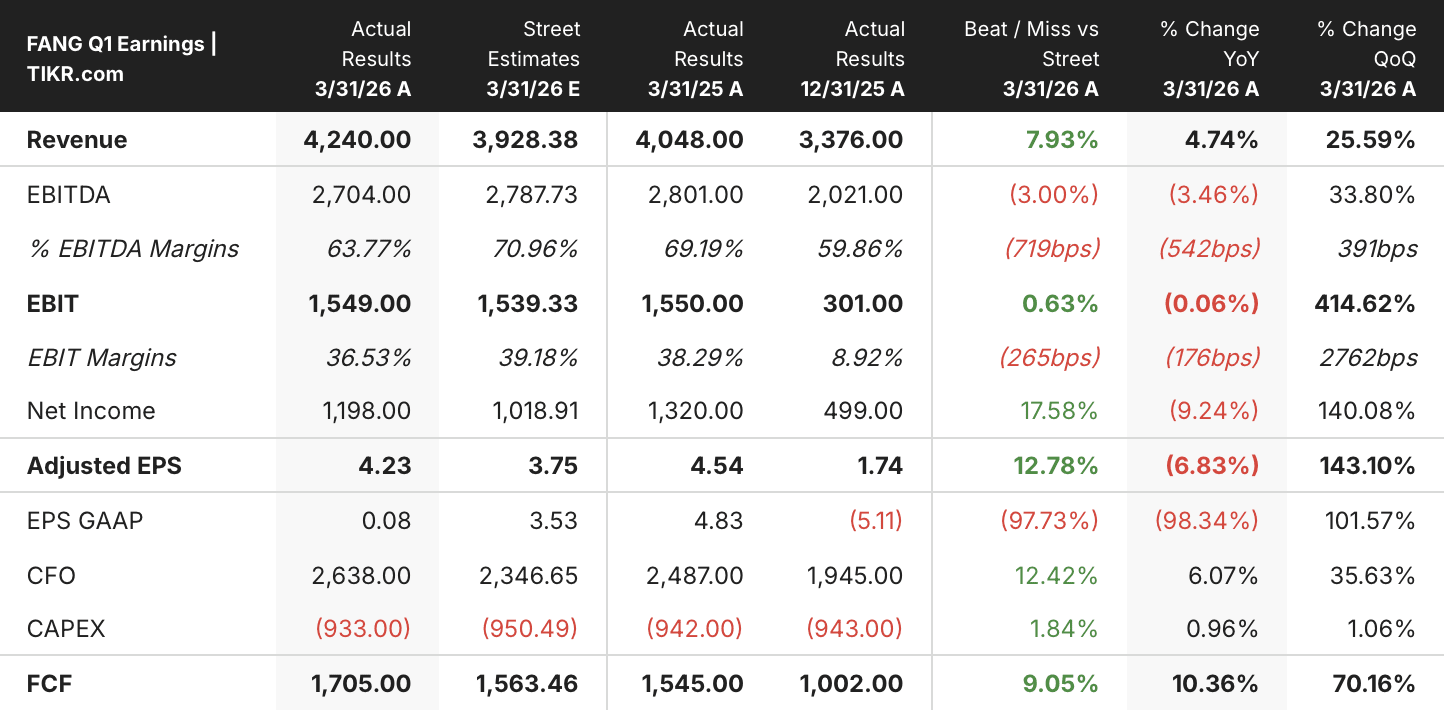

Free cash flow of $1.71 billion in Q1 2026 put Diamondback Energy (FANG) 9% above the $1.56 billion consensus estimate, but the TIKR valuation model assigns the stock a negative return through December 2030 even with that outperformance in hand.

FANG Stock Q1 2026 Earnings in USD (TIKR)

FANG Stock Q1 2026 Earnings in USD (TIKR)

The result landed against triple-digit oil prices and a global supply disruption that the company’s CEO described as the largest in history.

That FCF strength came from two compounding forces: oil production of 521,000 barrels per day exceeded guidance despite weather impacts, and capital expenditures of $933 million came in below the $950 million estimate. Together, those dynamics pushed the FCF margin to 40.2% for the quarter, up from 29.7% in Q4 2025.

Beneath the FCF headline, the quarter also delivered adjusted EPS of $4.23, beating the $3.75 Street estimate by around 13%, on revenue of $4.24 billion, which cleared the $3.93 billion consensus by around 8%. Adjusted EBITDA of $2.70 billion missed against the $2.79 billion estimate, with EBITDA margins compressing to 63.8% from 69.2% a year earlier.

The more important signal, though, was management’s response to the results. Addressing investors on the Q1 earnings call, CEO Kaes Van’t Hof tied the growth decision directly to Diamondback’s competitive position: “with the best inventory quality and depth in North America being executed at the best cost structure, if this isn’t the time to grow now, then I don’t know when it is.”

The company also moved from a yellow-light to a green-light framework, adding two to three rigs and a fifth completion crew for the remainder of 2026, raising full-year capital expenditure guidance to $3.9 billion from $3.75 billion.

What that acceleration means for cash generation is now the Street’s focus. CFO Jere Thompson outlined a path to $10 billion net debt within months, down from $12.7 billion pro forma.

The Q1 production beat triggered a specific debt paydown timeline and production ramp. See how the Street is updating its numbers. Track FANG analyst targets on TIKR for free →

Wall Street Rates Diamondback Energy Stock a Strong Buy with a $234 Mean Target

Street Analysts Target for FANG Stock (TIKR)

Street Analysts Target for FANG Stock (TIKR)

Wall Street rates Diamondback Energy stock with 25 buy or outperform ratings, 4 holds, and 0 sells as of late June 2026, reflecting near-unanimous bullish positioning following the Q1 print.

The mean price target sits at $234, implying around 30% upside from the current price of $180, with the high target reaching $277 and the low at $200.

The rating distribution has held stable since the Q1 earnings release, with no coverage downgrades recorded through the end of the June 2026 quarter.

Wall Street Projects Diamondback Energy’s Free Cash Flow to Peak Near $2.1 Billion in Q2 2026

FANG Stock FCF and FCF Margins Actuals & Estimates (TIKR)

FANG Stock FCF and FCF Margins Actuals & Estimates (TIKR)

Q1 2026 free cash flow of $1.71 billion arrived 10% above the year-ago $1.55 billion and 9% above the $1.56 billion Street estimate, confirming that Diamondback’s scale following the Endeavor integration is generating cash at a level above what consensus had modeled. The 40% FCF margin for the quarter marked a meaningful recovery from Q4 2025’s 30%, driven by the production outperformance and disciplined capital spend.

The Street now models Q2 2026 FCF at around $2.1 billion, a 24% sequential climb from Q1 actuals. Q3 2026 consensus sits at around $2.0 billion, with Q4 at around $1.8 billion, suggesting analysts expect the quarterly FCF peak to arrive mid-year before capital expenditures associated with the rig additions begin flowing through.

Looking into 2027, Q1 FCF consensus sits at around $1.7 billion and Q2 2027 at around $1.6 billion, both below the 2026 quarterly run rate. Those figures reflect a contracting FCF trajectory even as production continues to ramp, pointing to a commodity price assumption that the forward consensus does not extend at today’s levels indefinitely.

Bulls point to a $234 mean Street target anchored in today’s elevated FCF generation, while the TIKR model’s negative return implies the commodity environment producing those cash flows is cyclically elevated, with the outcome hinging on whether oil prices sustain above the mid-$60s WTI level management identifies as mid-cycle.

TIKR’s $160 Target on FANG Stock Signals That a Mid-Cycle Price Reset Is Not Priced In

TIKR’s mid-case model values Diamondback Energy at around $160 by December 2030, implying around 11% negative total return from the current price of around $180, or roughly 2.5% negative annualized over 4.5 years.

FANG Stock Valuation Model Results (TIKR)

FANG Stock Valuation Model Results (TIKR)

That return sits well below what energy investors typically require over a 4.5-year hold, and it stands in direct contrast to the Street’s $234 mean target.

The gap comes down to commodity assumptions. The TIKR mid-case models revenue at a negative 0.3% CAGR through 2035 and EPS growth of just around 1% annually, projecting that oil price normalization erodes the margins driving today’s 40% FCF performance.

TIKR’s mid-case targets $160 while the Street points to $234. The model inputs behind that gap are available on the platform. Build your own FANG valuation model on TIKR for free →

Should You Invest in Diamondback Energy, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Diamondback Energy, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Diamondback Energy, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FANG stock on TIKR for Free →

You May Also Like

Bitcoin-Backed Lending Market Shifts Toward Institutional Players, SVB Report Finds

68% of global BTC miners came from the U.S., Russia, and China, Q1 2026