This Stock is My Biggest Bet For July

The post This Stock is My Biggest Bet For July appeared first on 24/7 Wall St..

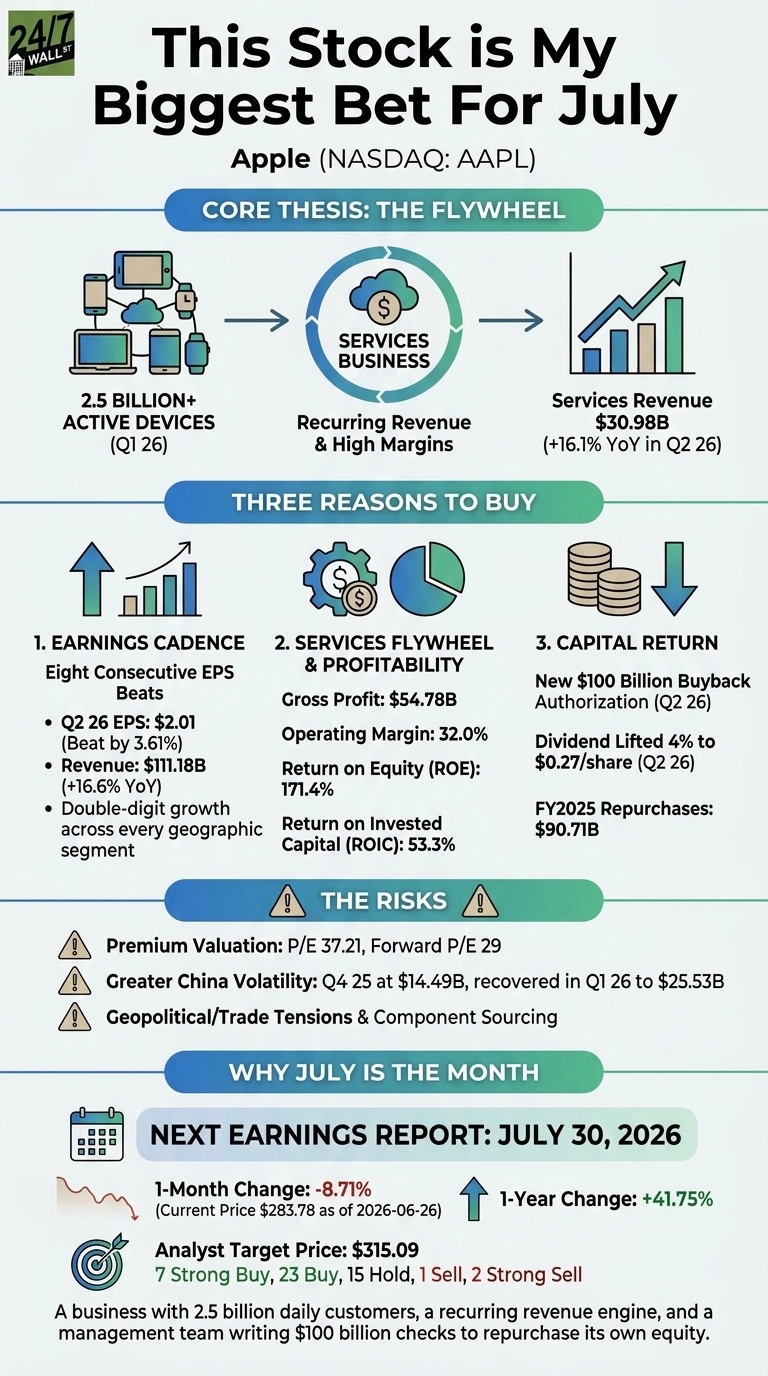

- Apple (AAPL) is a buy at $283.78 following an 8.71% pullback with strong earnings momentum and analyst targets of $315.09.

- Apple's Services business generates recurring software-margin revenues from 2.5 billion users locked into its hardware ecosystem.

- Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Apple didn't make the cut. Grab the names FREE today.

I keep hitting the buy button on Apple (NASDAQ:AAPL), and July is the month I am leaning in hardest. The pullback over the last month gave me the entry I wanted, and the catalyst I have been waiting on lands on the calendar in roughly four weeks. This is the position I have been adding to all year, and I am not done.

What pulls me back to the buy button is simple. Apple sells a device that 2.5 billion people refuse to put down, then rents them software, storage, music, and payments for the rest of their lives. The hardware locks them in. The Services business prints the rent. That is the entire thesis in two sentences, and every quarter the data hardens it.

The three reasons I keep buying

First, the earnings cadence. Apple has now posted eight consecutive quarters of EPS beats, with the most recent quarter delivering $2.01 against a $1.94 consensus. Revenue came in at $111.18 billion, up 16.6% year over year, with double-digit growth across every geographic segment. iPhone revenue alone hit $56.99 billion on what Tim Cook described as “extraordinary demand for the iPhone 17 lineup“. That is operational consistency I will pay up for.

Second, the Services flywheel. Services revenue reached $30.98 billion last quarter, growing 16.1% year over year, sitting on top of a gross profit of $54.78 billion and an operating margin north of 32%. Return on equity sits at 171.4% and return on invested capital at 53.3%. Those are utility-grade recurring revenues attached to luxury-grade margins.

Third, the capital return. The board approved a fresh $100 billion buyback authorization and lifted the dividend 4% to $0.27 per share. In fiscal 2025 alone, Apple repurchased $90.71 billion of its own stock. Every quarter I hold, my slice of the pie gets bigger without me lifting a finger.

The risk I will not pretend away

The valuation is rich. A P/E of 37 and forward P/E of 29 leave no margin for a stumble. Greater China is the other live wire. It cratered to $14.49 billion in the September 2025 quarter before snapping back to $25.53 billion in the December quarter. Tariffs, trade policy, and component sourcing out of Asia stay on my watch list every single day.

What keeps the thesis intact is the math underneath the multiple. Net income grew 19.36% last quarter, gross profit grew 22.1%, and operating cash flow in the December quarter jumped 80.14% year over year. When earnings compound faster than the multiple expands, the premium pays for itself.

Why July is the month

The next earnings report drops July 30, 2026, after the close. The stock is down 8.71% over the past month to $283.78, even though shares are up 41.75% over the past year and 1,232% over the past decade. Analysts polled on Wall Street currently carry a target of $315.09, with 7 Strong Buy and 23 Buy ratings against three sells.

24/7 Wall St.

24/7 Wall St.

I am buying a business with 2.5 billion daily customers, a recurring revenue engine that prints at software margins, and a management team writing $100 billion checks to repurchase its own equity. The buy button stays active for me through July, through the report, and through every quarter after it.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Apple didn’t make the cut. Grab the names FREE today.

The post This Stock is My Biggest Bet For July appeared first on 24/7 Wall St..

You May Also Like

Conservative columnist argues: Rubio could be more dangerous than Trump

Why this former OpenAI researcher thinks it’s time to start gaming out AI’s future