Teradyne Stock Fell 14% This Week in a Chip Rout. Is the Dip Worth Buying in 2026?

Key Stats for Teradyne Stock

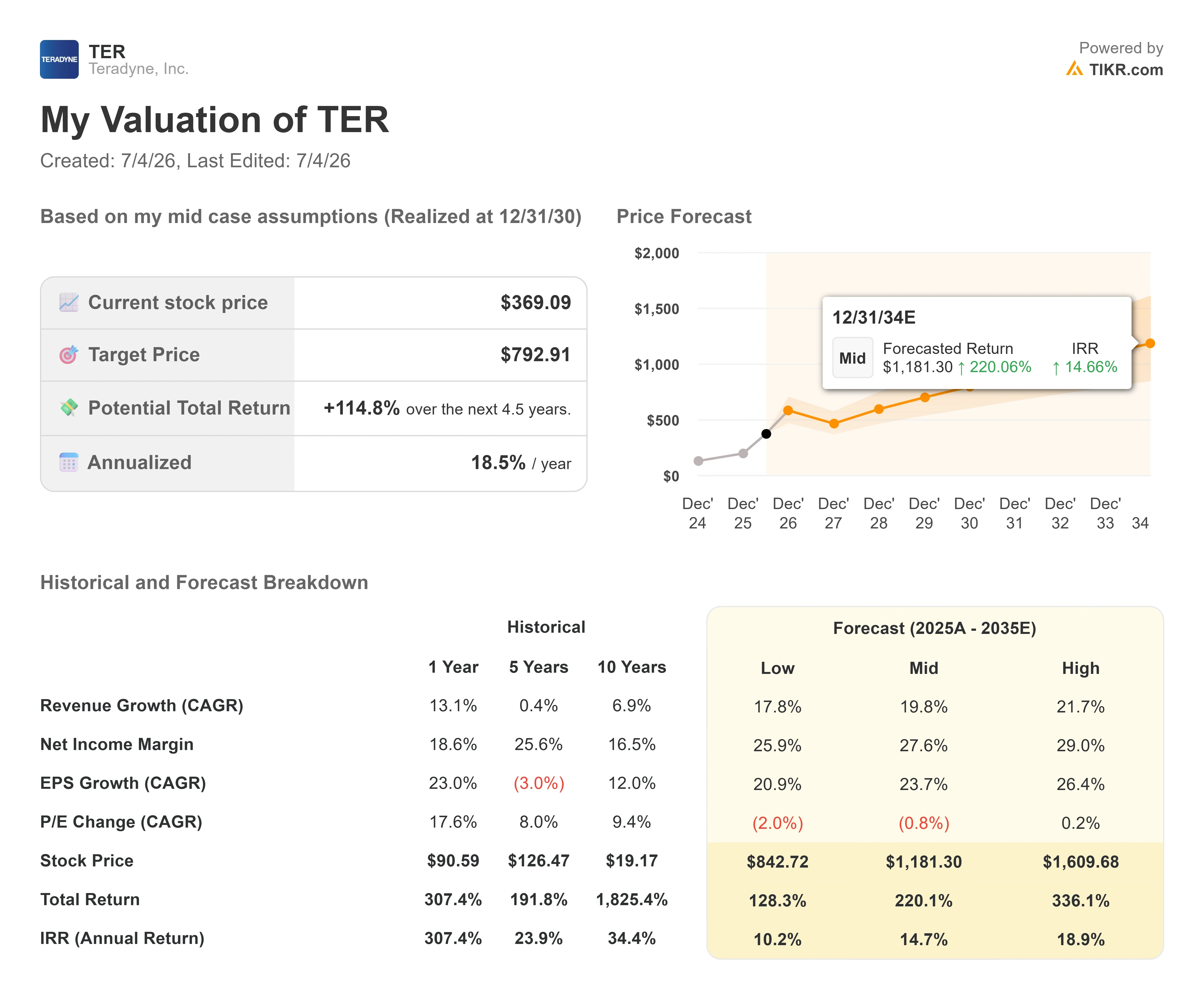

- Current Price: $369.09

- Target Price (Mid): ~$790

- Potential Total Return: ~115%

- Annualized IRR: ~19% / year

- Street Target: ~$417

- Earnings Reaction: -19.41% (April 28, 2026)

- Max Drawdown: -26.73% (April 29, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Teradyne (TER) did not do anything wrong on July 2. It just got sold anyway. The stock closed at $369.09, down 13.63% in a single session, one of the worst days the chip-test maker has had all year. There was no earnings miss, no guidance cut, no lost customer. The damage came from outside: a sector-wide panic over memory oversupply and stretched AI valuations that swept nearly every semiconductor name lower at once.

That is what makes Teradyne stock in 2026 an interesting question right now. For weeks the debate was whether the stock had run too far. It closed at a record $471.96 on June 25 and was still near $427 the day before this drop. Now it trades back below the Street’s mean target of roughly $417. The bulls spent the spring waiting for a reset. They may have just gotten one, delivered by news that had nothing to do with the company.

So the question flips. It is no longer “has this gone too far?” It is “is the fear rational, or is it handing you an entry?”

What actually knocked the stock down

The selloff was a group event, not a Teradyne event. On July 1 and July 2, memory and AI-related chip stocks tumbled together as investors reassessed whether the sector’s enormous run had outpaced the fundamentals. Reports that SK Hynix was slowing its high-bandwidth memory expansion revived an old fear: that aggressive capacity additions eventually tip the memory market into oversupply. Micron, a major Teradyne test customer, led the decline with a roughly 13% drop of its own.

The macro backdrop made it worse. Under new Federal Reserve Chair Kevin Warsh, markets have shifted toward pricing in higher rates rather than cuts, which pressures exactly the kind of high-multiple growth stock Teradyne had become. Higher discount rates hit future earnings hardest, and Teradyne was trading on a lot of future earnings.

Teradyne Drawdowns (TIKR)

Teradyne Drawdowns (TIKR)

The stat that frames the anxiety is valuation. Even after falling 14% on the week, Teradyne trades at an NTM (next twelve months, meaning the forward-looking estimate) EV/EBITDA of around 39x. That is a real premium, and it is the reason a memory scare hit this stock harder than the sector average.

See historical and forward estimates for Teradyne stock (It’s free!) >>>

Why the fundamentals point the other way

Here is the tension. The thing the market is afraid of, a memory glut, is the same thing that is supposed to drive Teradyne’s next leg of growth. More memory, especially HBM, means more testing, and testing is what Teradyne sells.

CEO Gregory Smith made the mechanism explicit at the Bank of America 2026 Global Technology Conference on June 2. Talking about DRAM going into HBM, he said “the test intensity for that is much higher because of the stacking and the quality requirements downstream.” The same logic applies to AI accelerators. As Smith put it, when you stack “2 big compute die plus 6 HBM stacks plus a CoWoS interposer, the cost of having a failure downstream is so high that you’re willing to invest to get to a higher level of test quality upstream.” That is why a memory boom is supposed to become a Teradyne tailwind rather than a threat.

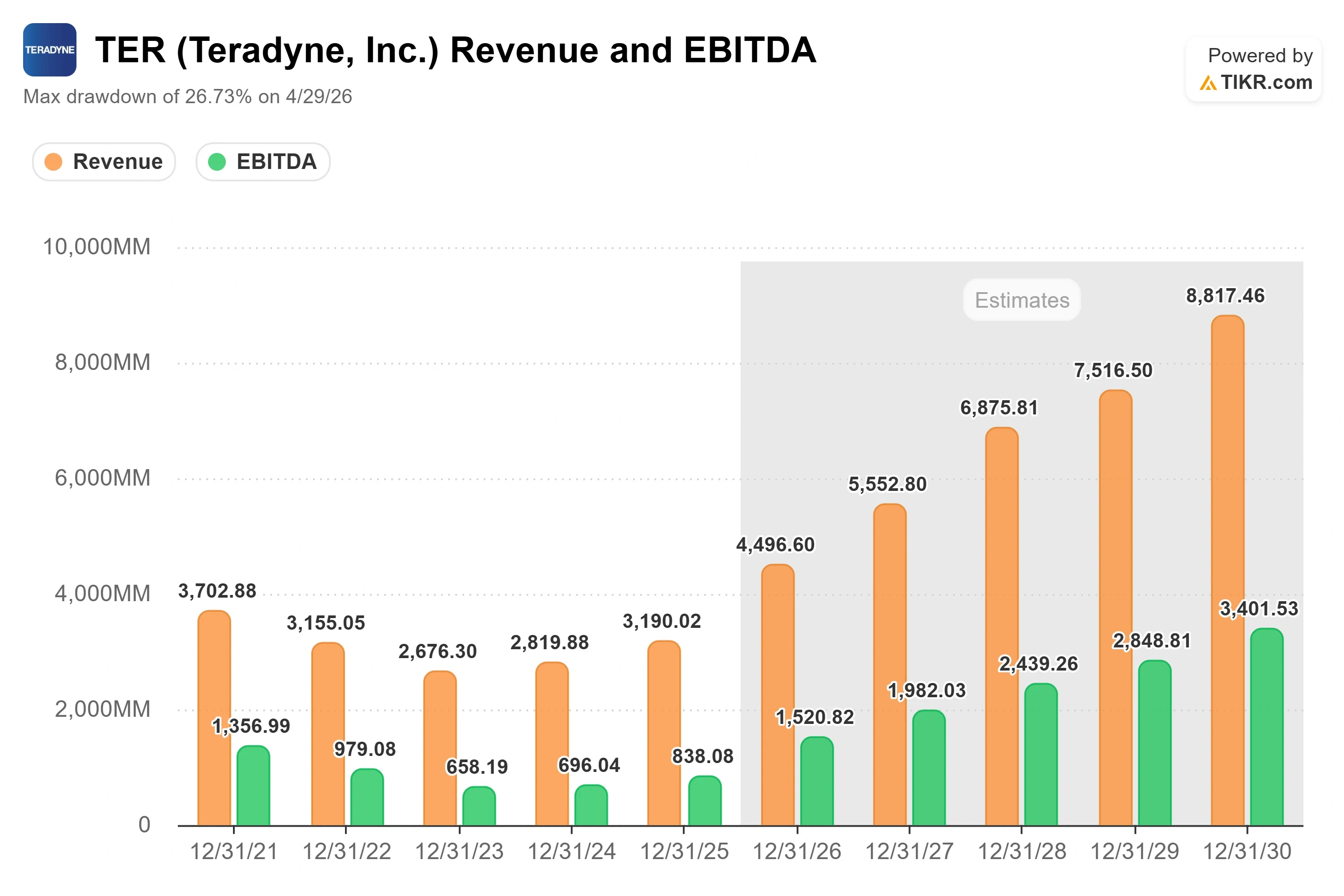

Smith also laid out the size of the prize. He framed the automated test equipment, or ATE (the machines that check whether a finished chip actually works), market growing from about $9 billion in 2025 toward $12 billion to $14 billion, with Teradyne positioned to reach roughly $6 billion in revenue, close to double its 2025 base. That comes from both a bigger market and share gains inside it. Teradyne’s ATE share sat around 30% in 2025, and Smith expects 35% to 38% in that larger market as the company claws back share in compute and DRAM that it lost during the mobile-to-AI shift. That matters because it reframes the stock as an early-innings share gainer, not a peak-cycle bet.

Teradyne Revenue & EBITDA (TIKR)

Teradyne Revenue & EBITDA (TIKR)

The near-term numbers back the story so far. Q1 2026 was the best quarter in company history: revenue of $1.282 billion, up 87% year over year, with non-GAAP EPS of $2.56. Teradyne has now beaten revenue estimates for five straight quarters. The catch, and the reason the stock is volatile, is that management guided Q2 revenue to $1.15 billion to $1.25 billion, a step down from the Q1 record, and has flagged limited visibility into the back half. The market already punished that lumpiness once: despite the record Q1 beat, TER fell 19.41% the day after its April 28 report.

On peers, the premium is real but not absurd for the growth. Teradyne’s roughly 39x NTM EV/EBITDA sits above test rival Advantest at about 29x and Applied Materials near 35x, though closer to KLA at around 41x. The question the model has to answer is whether roughly 20% forward revenue growth and mid-20s EPS growth justify paying up.

See how Teradyne performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $369.09

- Target Price (Mid): ~$790

- Potential Total Return: ~115%

- Annualized IRR: ~19% / year

Teradyne Advanced Valuation Model (TIKR)

Teradyne Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Teradyne stock (It’s free!) >>>

This uses TIKR’s mid-case scenario, realized at year-end 2030. It is the right case here because the whole debate is whether the AI-testing cycle is durable, and the mid case assumes it plays out without demanding the aggressive high-case outcome.

The model points to a target of about $790, an annualized return of roughly 19% per year over the next 4.5 years. Two revenue drivers carry it: the ATE market expansion toward $12 billion to $14 billion, and Teradyne’s share gains in AI compute and HBM testing. The margin driver is operating leverage on a largely fixed cost base, which pushes net income margin from the high teens toward the high 20s as revenue scales. The primary risk is customer concentration, because a handful of large hyperscalers and memory programs drive the order book, and a single delay creates exactly the “peaks and valleys” Smith has warned about. The upside case is that HBM and merchant GPU demand convert to booked orders and the roughly 19% annualized return compounds. The downside case is that a real memory glut arrives, orders stall, and the premium multiple compresses fast.

Conclusion

The July 2 drop reset the price, not the thesis. Nothing about Teradyne’s business changed on the day its stock fell 14%. What changed is that the stock now sits back below the Street’s mean target, a very different starting point than the record it hit a week earlier.

The catalyst that settles it is the Q2 2026 earnings report, expected after the close on July 28. Watch the full-year framing, not the headline number. Good looks like management holding or raising its full-year target while confirming that memory and HBM orders are actually building in the backlog. Bad looks like an in-line print, no raise, and more cautious back-half language that hands the memory-glut bears their proof. Remember what happened last time: the stock dropped more than 19% after a record beat because guidance, not the result, set the tone. Mark July 28. This time, the reaction may tell you more than the print.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Teradyne?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Teradyne, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Teradyne alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Teradyne on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Lawyers remain in disbelief over ‘fascist Hellscape’ July 4 display in DC

LIST: Bayanihan initiatives amid soaring oil prices

Trump's billion-dollar crypto gain came with almost $4B investor losses