BitMEX Highlights How Traders Can Profit From Funding Rate Differences Between Different Perps Platforms

Key highlights:

- BitMEX’s Q2 2026 Derivatives Report identifies three structural drivers of funding rate disparities in perpetual futures markets

- The report says differences in collateral type, exchange user bases, and index mechanics can create recurring trading opportunities

- The report outlines three trade ideas involving BTC perpetuals, Hyperliquid-Binance spreads, and WTI commodity perpetuals

BitMEX has released its Q2 2026 Derivatives Report, Three Sources of Funding-Rate Alpha, examining why funding rates can differ across otherwise similar perpetual futures contracts.

According to BitMEX, funding rates are not only a reflection of short-term market sentiment. The report argues that persistent differences can emerge from structural factors such as margin currency, exchange demographics, and oracle or index design.

BitMEX CEO Peter Wilkinson commented on the nuances affecting funding rates:

Three sources of funding rate disparities

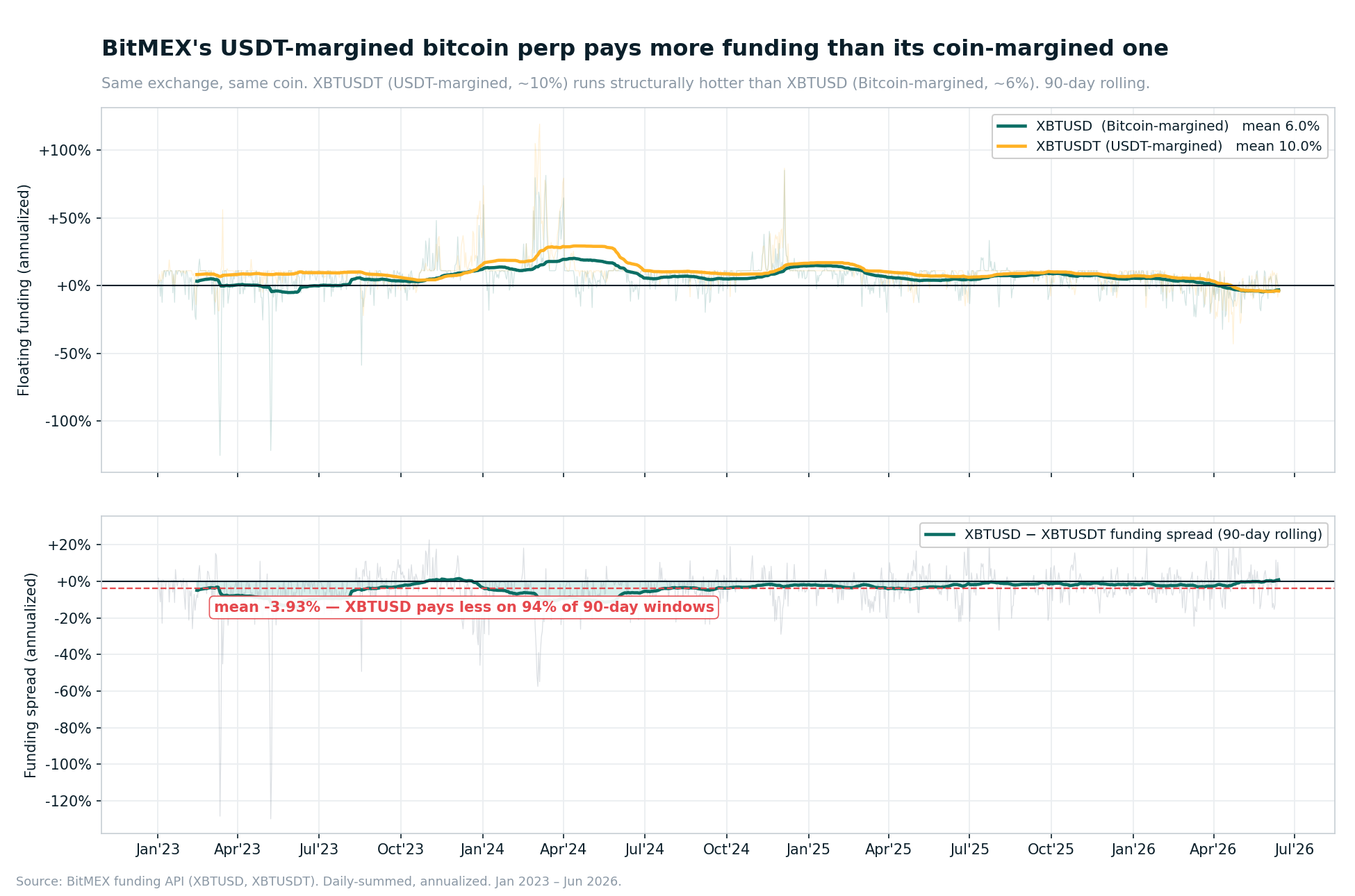

The first source highlighted by BitMEX is margin design. The report compares BitMEX’s bitcoin-margined XBTUSD contract with its USDT-margined XBTUSDT contract, finding that the funding spread between the two averaged approximately -3.93% annualized over the past three and a half years and remained negative in 94% of rolling 90-day periods.

Source: BitMEX

BitMEX says the gap reflects the different trader profiles attracted by each collateral type. BTC-margined contracts tend to attract traders who already hold Bitcoin and may use the product to hedge, while USDT-margined contracts tend to attract traders looking to deploy stablecoin capital for leveraged long exposure.

The second source is exchange demographics. BitMEX found that Hyperliquid’s Bitcoin perpetuals generated an average annualized funding premium of 7.17% over Binance between 2023 and 2026, while Ether perpetuals showed a 5.31% premium. The report attributes the difference partly to Hyperliquid’s more retail-oriented, on-chain user base and the operational barriers that can limit institutional arbitrage on decentralized venues.

The third source is oracle and index design. In commodity perpetuals such as crude oil, BitMEX says futures-based indexes can create sharp funding distortions during contract rolls. The report notes that BitMEX’s WTIUSDT funding rate briefly fell to around -531% annualized during an April 2026 futures roll, illustrating how index construction can influence funding independently of broader market sentiment.

Three trade ideas highlighted in the report

Arbitraging funding rate differences on BitMEX's XBTUSD and XBTUSDT contracts

BitMEX’s first trade idea focuses on the difference between its XBTUSD and XBTUSDT contracts. A trader could go long XBTUSD and short XBTUSDT, reducing Bitcoin price exposure while attempting to capture the funding spread between the two markets. BitMEX says Multi Asset Margining can make the trade more capital-efficient by allowing both legs to be backed by a single collateral pool.

Taking advantage of the funding spread between Hyperliquid and Binance

The second trade idea involves cross-exchange funding spreads between Hyperliquid and Binance. Since Hyperliquid’s BTCUSDT and ETHUSDT perpetuals have historically shown higher funding than Binance’s comparable contracts, a trader could short the higher-funding Hyperliquid perp and go long the lower-funding Binance perp to collect the structural premium while hedging directional exposure.

Arbitraging WTI Crude perpetuals on BitMEX and the CME

The third trade idea relates to WTI commodity perpetuals. BitMEX describes a theoretical trade involving a short position in WTIUSDT and a long position in the corresponding CME futures contract, but notes that funding costs can offset much of the basis profit. As a result, the report suggests that traders may be better served by focusing directly on the funding rate rather than relying on spot-futures convergence.

The bottom line

BitMEX concludes that funding rate gaps are often driven by market structure rather than sentiment alone. While these disparities can create opportunities, the report stresses that traders should first identify the source of the funding difference and account for risks such as basis shifts, liquidity constraints, collateral requirements, and venue-specific execution issues.

You May Also Like

Cathie Wood’s ARK Invest Buys $13.7M in Circle Shares While Selling Robinhood Stock

The changing face of elder care in Malaysia — Sayed Mohammad Reza Yamani Sayed Umar

Not a loophole: Singapore AI export controls let China tap US AI legally