SBF Reignites Debate, Claims FTX Was Never Bankrupt and Could Have Repaid Everyone

TLDR

- SBF claims FTX had $25B in assets, enough to repay all user obligations.

- Legal teams allegedly forced a premature Chapter 11 bankruptcy on FTX.

- Report says asset mismanagement led to undervaluation and forced sales.

- Crypto holdings reportedly exceeded liabilities, making bankruptcy avoidable.

- Market reactions and pardon rumors add fuel to FTX’s ongoing controversy.

A new document posted via Sam Bankman-Fried’s X account reignited the FTX Bankrupt controversy. The report argues that the exchange never needed to file for bankruptcy and had enough assets to repay users. It challenges the legal narrative and pushes claims that legal counsel forced an unnecessary Chapter 11 filing.

SBF Alleges Legal Missteps Caused Bankruptcy Filing

Sam Bankman-Fried now claims that FTX was never bankrupt and blamed legal teams for initiating Chapter 11 unnecessarily. The report posted on X alleges the company had sufficient assets and liquidity to repay users. It states FTX had $25 billion in assets against $8 billion in customer obligations at the time.

He argues legal advisers ignored internal records and asset valuations and proceeded with bankruptcy filings prematurely. The 15-page report claims FTX’s new management team mishandled the asset recovery process. It also asserts lawyers were financially motivated to push for the bankruptcy filing.

Furthermore, the report emphasizes that the legal team undervalued FTX’s assets and sold them at below-market prices. The report estimates those assets would now be worth over $136 billion if retained. It blames advisors for discarding $7 billion in FTT and other key investments.

Crypto Holdings Valued Higher Than Liabilities

Bankman-Fried’s report lists major holdings that allegedly exceeded the company’s debts, suggesting FTX was never bankrupt. Assets included 58 million SOL, 205,000 BTC, and large stakes in Robinhood, Ripple, and Anthropic. These were said to be enough to cover user withdrawals and preserve exchange operations.

He insists that the crisis was only a liquidity issue and could have been resolved without invoking bankruptcy. According to the document, the company required more time and internal restructuring. However, external forces allegedly accelerated the bankruptcy process, causing lasting financial damage.

The report also claims that repaying users was feasible from the start, with assets sufficient “in full, in kind.” Legal fees amounting to $1 billion and consultant charges are blamed for asset depletion. Despite the legal process, the estate reportedly still holds $8 billion in surplus.

Public Reaction and Market Response Stir Controversy

The report’s release caused the FTX Token to spike to $0.84 before cooling off within hours. Crypto analysts criticized the claims and warned against misinformation surrounding the FTX Bankrupt case. Many rejected the mark-to-market arguments, pointing to 2022 asset prices during the bankruptcy.

Critics also noted that repayments were based on lower valuations at the time of collapse, not current prices. Allegations of asset underutilization and forced liquidation added fuel to online debates. While some users supported SBF’s claims, others criticized him for signing the bankruptcy documents.

Political elements entered the picture as reports emerged of a pardon campaign for Bankman-Fried. Sources claimed his allies are lobbying for a Trump pardon, drawing parallels to recent pardons of crypto figures. This campaign has raised questions about the timing and purpose of the new FTX Bankrupt report.

Fraud Conviction and Appeal Ongoing

Sam Bankman-Fried was convicted in 2023 on multiple fraud and conspiracy charges related to FTX’s collapse. Prosecutors proved that Alameda Research misused customer funds via a secret backdoor, bypassing FTX’s risk engine. This ultimately triggered a mass withdrawal event and exposed an $8 billion hole.

Following the FTX Bankrupt filing in November 2022, Bankman-Fried was arrested in the Bahamas. He is currently serving a 25-year prison sentence and has launched an appeal. His latest claims seek to rewrite the FTX narrative and question the legitimacy of the bankruptcy process.

Despite widespread skepticism, the report has renewed scrutiny over FTX’s asset management. The crypto community remains divided, with some raising concerns over legal accountability. Bankman-Fried’s push to revise the FTX Bankrupt story shows no signs of slowing down.

The post SBF Reignites Debate, Claims FTX Was Never Bankrupt and Could Have Repaid Everyone appeared first on CoinCentral.

You May Also Like

Q2 Market Insights: Bitcoin regains dominance in risk-averse environment, ETFs remain critical to market structure

Hedera Price Prediction Holds Bullish as Iran Peace Deal Pushes Bitcoin Above $65,000 and Pepeto Presale Passes $10 Million

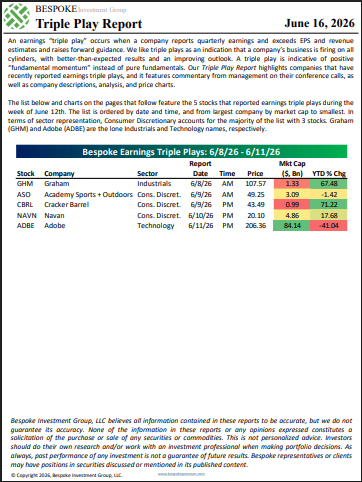

The Triple Play Report: 6/16/26