Fiat-to-Crypto Gateways: A Cornerstone of Mass Adoption

By Pauline Shangett, CSO at ChangeNOW

Every financial revolution starts quietly, not with headlines, but with infrastructure. Crypto is no different. Beneath the noise of token prices and regulatory skirmishes, a deeper transformation is unfolding: the global wiring of money is being rewritten in real time. Because in the end, crypto adoption was never really about the coins, It was more about the bridge

The invisible but critical stretch between your bank balance and your wallet, between dollars and digital tokens. That’s where the real war for the future of money is being fought, and lately, the legacy players, the JPMorgans, Visas, and Mastercards of the world, have quietly crossed that bridge themselves.

They’re not just peeking over the fence anymore; they’re wiring it, and the message is clear: tokenized cash, whether it’s stablecoins, CBDCs, or bank-minted digital money, isn’t some niche experiment. It’s the next-generation plumbing of finance.

Call it what it is: a full-scale revolt against latency, opacity, and fees. Because once money moves in seconds, not days, the entire justification for SWIFT, correspondent banks, and the endless intermediaries of the “trusted” old world starts to crumble.

McKinsey wasn’t exaggerating when it said tokenized money “has the ability to clear good funds and settle a payment almost instantly.” That’s not a minor upgrade. That’s a sledgehammer to the foundation of global finance.

The Old Guard Just Blinked

You can almost feel the shift in the air. JPMorgan’s high-profile partnership with Coinbase in mid-2025 wasn’t a press stunt; it was a declaration. The biggest U.S. bank, with 80+ million customers, is now hand-delivering on-ramps to crypto directly from the same cards, accounts, and loyalty points people already use.

Starting this fall, Chase cardholders can buy crypto on Coinbase as easily as they buy coffee: no extra steps, no third-party apps, and no janky interfaces. Next year, they’ll be able to convert their Chase Ultimate Rewards points straight into USDC, turning loyalty into liquidity. And by 2026, bank account links will make fiat-to-crypto transfers instant.

So much for “banks are scared of crypto.” They’ve realized what the rest of the market has known for years: the future of money isn’t about speculation; it’s about frictionless movement.

Visa’s Quiet Revolution: Turning Stablecoins Into Everyday Money

While the banks make headlines, Visa has been quietly rebuilding the payment infrastructure from the inside out. The company’s 2025 updates read less like a fintech roadmap and more like a manifesto.

Visa now supports multiple stablecoins like USD, EUR, and more across several blockchains. In July 2025 alone, it added Paxos’ Global Dollar, PayPal USD, and Circle’s EURC, while expanding settlement compatibility to Stellar and Avalanche.

But let’s take a closer look at a real move – stablecoin-linked cards. These let consumers spend directly from their stablecoin balances at 150+ million merchants worldwide. Visa’s tokenization platform can mint, burn, and transact stablecoins natively, meaning your digital USDC wallet can tap into the same payment rails that move trillions in fiat every year.

Faster cross-border payments. Lower fees. Round-the-clock settlement. All without ripping out your existing systems. So while regulators debate “crypto integration,” Visa’s already doing it.

Mastercard: Playing Offense in the Stablecoin Era

If Visa is the quiet architect, Mastercard is the bold disruptor with a suit on. In mid-2025, it joined the Paxos Global Dollar Network, a consortium for regulated stablecoins, and began enabling USDG, USDC, PYUSD, and FIUSD across its entire payment ecosystem.

In simple words, banks and wallets using those stablecoins can now plug directly into Mastercard’s rails. Stablecoin issuance, card payments, and cross-border remittances – all connected.

But here’s where it gets spicy: Mastercard didn’t stop at acceptance. “Mastercard Move,” its cross-border platform, now handles stablecoin flows directly. “One Credential” will soon let consumers spend fiat and stablecoins interchangeably, blurring the line between legacy balances and on-chain liquidity.

There is also a partnership with Chainlink that enables direct crypto purchases on decentralized exchanges. For example, if you buy tokens on Uniswap using your Mastercard, Chainlink will convert the fiat payment into an on-chain swap.

When the first person buys Bitcoin on a DEX using their credit card, it won’t be a hacker. It’ll be your neighbor. And it’ll probably say “Mastercard” on the receipt.

Europe Strikes Back: A Euro Stablecoin Consortium

Meanwhile, Europe, often accused of lagging behind in the digital asset race, is quietly engineering its comeback. In September 2025, nine major banks, including ING, UniCredit, Santander, and Danske Bank, announced a new Netherlands-based company to issue a euro-denominated stablecoin.

MiCA-compliant, e-money licensed, and backed by the continent’s biggest institutions, it’s expected to launch in 2026. The goal is to create a trusted European payment standard that runs 24/7, settles instantly, and reduces dependence on U.S. infrastructure.

So Europe is tired of relying on American stablecoins and dollar rails. By launching its own euro stablecoin, the consortium is essentially saying, “If we can’t beat the crypto rails, we’ll build on them.”

Each member bank plans to wrap new services like custody, wallets, and compliance around this stablecoin, turning it into more than a currency. It’s a statement. And ING’s projection says it all: “24/7 instant cross-currency settlement.”

Legacy Europe is finally learning the crypto lesson: the future doesn’t wait for business hours.

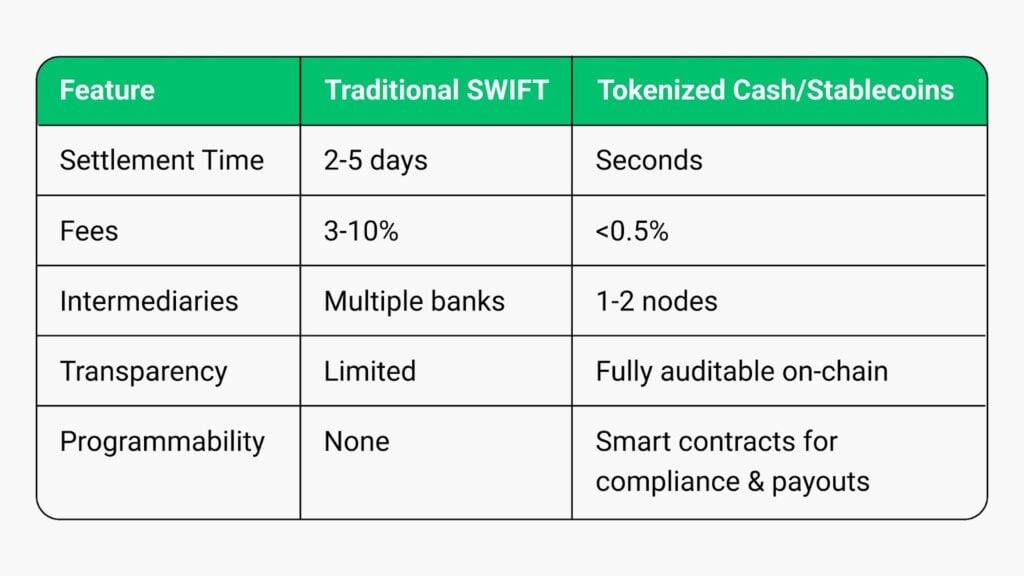

Tokenized Cash vs. the Old Rails: The Inevitable Showdown

At the heart of all these moves lies a brutal truth: the infrastructure we use to move money is prehistoric.

SWIFT transfers take between one and five business days. Each hop between correspondent banks adds costs, delays, and risk. The process is opaque by design, a holdover from an era when “trust” meant “trust us, we’ll handle it.”

Now contrast that with blockchain. Payments settle in seconds, and systems run 24/7. Transactions are transparent, auditable, and programmable, that last part is key, programmability.

Money as code. That’s the paradigm shift. Imagine transfers that automatically enforce escrow conditions, FX conversions, or compliance checks, all embedded at the transaction layer.

We’re not talking theory anymore. Analysts have already shown that tokenized payments can auto-run AML/KYC checks mid-transfer. No back-office middlemen, no overnight batch processing, just real-time compliance on programmable money.

This is why Visa, Mastercard, and JPMorgan aren’t just “experimenting.” They’re rewriting their core systems. We’re watching the old rails of global commerce being refitted with blockchain infrastructure, a stealth revolution that will make SWIFT look like dial-up.

A World of 70+ Fiat-Backed Digital Tokens

And this isn’t limited to the U.S. or Europe. The tokenization wave is everywhere.

Triple-A, a payments compliance firm, now enables crypto settlements across 90+ countries and over 70 fiat currencies. Their infrastructure allows local businesses to convert directly into stablecoins, bypassing legacy banks entirely. That’s not an edge case; that’s the new trade finance model in action.

Central banks are catching on, too. China’s e-CNY pilot, the EU’s digital euro project, and a growing list of Caribbean and African CBDCs all point to the same conclusion: the fiat-to-crypto divide is collapsing.

Every new stablecoin and every new tokenized fiat adds another node to the global network. USD, EUR, BRL, IDR, you name it. We’re moving toward a world where a Brazilian exporter could receive BRZ (a tokenized real) in seconds from a European buyer paying in euro stablecoins.

No SWIFT. No intermediaries. No “business days.”

The numbers back it up: annual on-chain settlement volumes have already topped $30 trillion, putting blockchain payment activity in the same league as Visa or SWIFT. Let that sink in. The supposed “fringe rails” of crypto are already processing at a scale comparable to the incumbents they were meant to disrupt.

The Inevitable Convergence

So where does this all lead? Toward an uncomfortable truth: tokenized cash isn’t replacing money, it’s replacing the plumbing. The wires, the rails, the clearinghouses. The bureaucracy we’ve accepted as the “cost of safety.” It’s being refactored, line by line, into software.

And for all the hand-wringing from traditionalists, this isn’t chaos. It’s evolution. Stablecoins and CBDCs reinforce the best parts of legacy finance, trust, compliance, universality, while stripping out the inefficiency.

Visa and Mastercard get it. JPMorgan gets it. The European banks finally get it. The only question is: who doesn’t?

For businesses, this shift isn’t optional. Treasury departments will need to adapt to 24/7 liquidity. Cross-border payments will no longer take a week; they’ll take seconds. Regulators will need to supervise not just transactions but code.

And for crypto-native platforms, ChangeNOW, for example, this is the golden moment. As liquidity fragments across hundreds of fiat tokens and stablecoins, someone needs to connect it all. To become the universal translator between every flavor of digital cash.

The Final Thoughts

Money has always been political. The infrastructure behind it, who clears it, who approves it, and who profits from it, defines power. Tokenized cash doesn’t change that dynamic; it redistributes it.

The nations, banks, and companies that adapt will control the new rails of the digital economy. The ones that cling to the old system will find themselves like postal carriers in the age of email, still delivering, but irrelevant. What we’re seeing isn’t just “crypto adoption.” It’s the quiet standardization of global value transfer on open protocols. And it’s happening faster than most people realize.

Because at the end of the day, the average person doesn’t care about whether a payment is “on-chain” or “off-chain.” They care that it’s instant, cheap, and always on. The moment crypto rails make that invisible, mass adoption becomes inevitable. The fiat-to-crypto gateway isn’t a side feature. It’s the cornerstone of the new financial order.

So yes, the old system will resist. SWIFT will lobby. Regulators will stall. Headlines will fret about “risk.” But none of it matters. Because once the infrastructure exists, once people taste real-time, 24/7, borderless payments, there’s no going back.

The bridge between fiat and crypto isn’t just opening. It’s becoming the main highway. And soon, you won’t even notice when you’ve crossed it.

You May Also Like

US Dollar Gains Ground as Retail Sales Hold Up, Yields Rise

Exclusive interview with Smokey The Bera, co-founder of Berachain: How the innovative PoL public chain solves the liquidity problem and may be launched in a few months