Liquidity Wars Wipe Out Billions: DWF Labs’ Andrei Grachev Sounds the Alarm

Andrei Grachev, managing partner at DWF Labs and a founding partner of Falcon Finance, published a pointed thread on X this week that reads less like a marketing note and more like a market wake-up call. In the post, he calls the current turmoil “Liquidity Wars,” argues that many so-called synthetic dollars are misunderstood by users, and lays out a string of policy changes at Falcon Finance meant to steer the company away from the risky growth tactics that, he says, have amplified recent losses.

Grachev’s central claim is blunt. Recent liquidations have already erased tens of billions of dollars from the crypto market, even without a headline collapse on the scale of FTX. He points to the industry’s tendency to label complex yield products “USD-something,” creating an illusion of cash-like safety that breaks down under stress. “Synthetic dollars are not stable coins like USDt, they are a dollar weighted representation of the underlying assets, risk management and trading strategies,” he wrote, warning that using those instruments as collateral for highly leveraged positions turns the question of failure from “if” to “when.”

The warning is grounded in recent market events. Data aggregators and market reporters logged extraordinary forced liquidations in October and early November, with one brutal day when more than $19 billion in positions were liquidated during a cascade of margin calls. Industry trackers such as Coinglass have shown extreme spikes in liquidations across exchanges, and mainstream outlets reported the October cascade as the largest single-day liquidation event on record. Grachev’s figure, “more than $22 billion liquidated in the last 31 days,” sits alongside those observations as part of a month of recurring volatility and mass deleveraging.

Lessons After Massive Liquidations

Beyond numbers, Grachev’s post is a critique of business models that prioritize TVL, token farming and marketing growth over real sustainable profitability. He likens current product design and go-to-market behavior to a cargo-cult: projects replicate the trappings of success, rich lending markets, many farming pools, looping rewards, without a durable financial rationale, he says, leaving leveraged TVL that can “disappear in a moment.” Such looping strategies and special curator deals, he argues, damage true profitability because they constrain how assets can be used in trading and hedging.

Grachev also used the post to make public what he described as a strategic pivot for Falcon Finance, the synthetic dollar and collateralization protocol backed by DWF Labs. He announced the immediate end of special marketing deals with TVL contributors, a sharp reduction in token-based marketing that allocates $FF for retail distribution, and the elimination of special redemption privileges or curator advantages.

Instead, Falcon will focus on institutional and retail clients seeking yield with no leverage risk, on real-world asset adoption, and on strategies designed to be unwindable quickly with limited basis exposure. Those moves, Grachev suggested, are meant to prioritize credibility and resilience over short-term growth metrics. Falcon’s public materials have described USDf as an overcollateralized synthetic dollar aimed at providing yield while serving as an on-chain buffer between volatile crypto and dollar stability.

The post touches on familiar fault lines in crypto’s history. Grachev explicitly reminds readers that high-profile, heavily underwritten projects previously endorsed by reputable investors and institutions have still failed, citing FTX and Terra/Luna as cautionary examples of reputation not being a substitute for robust financial architecture. His argument is that institutional logos, media presence and conference stage appearances do not immunize a product from market mechanics.

Analysts and market participants will watch closely whether other protocols follow Falcon’s de-emphasis of TVL and token incentives in favor of balance-sheet strength and transparent risk management. Some industry observers say the month’s liquidations have already forced a broader reappraisal: leverage and tokenized yield loops amplified the sell-off, and now projects that can demonstrate real income, quick unwind capability and genuine collateralization may attract capital.

Grachev ends his thread with an oddly optimistic note. He allows that crypto has grown and is still offering “great opportunities,” tokenized real-world assets, BTC and selective altcoin strategies, and DeFi native yields, but insists the industry must get its risk framing right. “Every storm creates opportunities, and we should be grateful that we live in a time of opportunities,” he wrote, closing with the familiar investor admonition: DYOR, not financial advice. Whether that call for sobriety signals a broader sea change in how protocols design yield and TVL remains the big open question for the weeks ahead.

You May Also Like

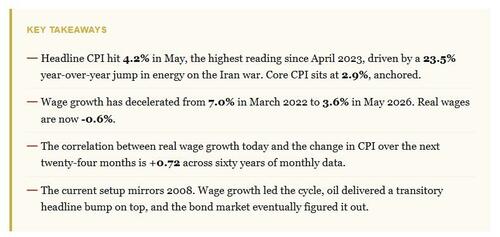

Wage Growth As A Leading Inflation Indicator

Retail Veteran Mitch Gould’s Distribution Platform Addresses Growing Complexity in U.S. Sports Nutrition Market

USA vs Belgium Odds: World Cup 2026 Win Probability and MEXC Prediction Market Guide