Why Venture Capital Is Pouring Into On-Chain Neobanks in 2026: Crypto Finally Grows Up

The crypto industry has entered a new phase: investors are no longer chasing the shiniest new protocol or triple-digit yields. Instead, billions are flowing into a fast-emerging category—on-chain neobanks—consumer-focused platforms that make decentralized finance feel as simple as Venmo or Revolut while keeping full self-custody.

This pivot marks the moment crypto moves from speculation to actual utility.

The Core Problem Crypto Still Hasn’t Solved: Usability

After a decade of explosive innovation—Layer 1s, Layer 2s, DeFi summer, NFT mania, restaking, and real-world assets—one glaring truth remains:

Most people still can’t use crypto without a PhD in blockchain.

Bridging assets, managing gas fees, approving endless smart-contract interactions, and juggling multiple wallets remain major barriers for mainstream users. While power users thrive, the average person gives up after the first confusing step.

Savvy investors now see this friction not as a temporary inconvenience, but as the single biggest bottleneck to trillion-dollar adoption.

Capital Is Now Betting on Abstraction, Not New Primitives

2025–2026 funding trends tell the story clearly:

VCs have stopped funding the 47th lending protocol or the 23rd liquid-staking derivative. Instead, they’re backing companies that sit on top of existing infrastructure and hide the complexity.

These on-chain neobanks aggregate liquidity across chains, automate gas and bridging, embed smart-account abstraction (ERC-4337), and deliver one-tap experiences for earning yield, spending stablecoins, or borrowing against crypto collateral.

Recent standout raises in this category:

- Veera – $10M+ for its mobile-first on-chain banking app with built-in Financial Identity Score

- Similar rounds for apps like Lava, Soul, Porta, and others now in stealth

Investors are explicitly saying:

From Yield Chasing to Everyday Financial Habits

Previous DeFi growth was almost entirely incentive-driven. Users farmed tokens, yields collapsed, TVL vanished.

The new generation of on-chain neobanks flips the model. They focus on sticky, daily behaviors:

- High-yield stablecoin savings (but with auto-compounding and no manual claiming)

- Crypto debit cards with cashback paid in BTC or ETH

- Instant cross-border payments

- Payroll direct deposit into self-custodial wallets

- Under-collateralized lending powered by on-chain credit scores

These products create retention that survives bear markets because people use them even when prices are flat or falling.

On-Chain Identity: The Missing Piece Traditional Finance Can’t Offer

As these platforms begin offering lending and risk-based products, they face the same question banks do: How do you underwrite users without centralized credit bureaus?

The answer emerging in crypto: privacy-preserving, portable on-chain reputation systems.

Veera’s Financial Identity Score, for example, combines verified off-chain data (KYC when needed) with on-chain transaction history to generate a dynamic credit profile users actually own and can take across platforms.

This is potentially revolutionary for the estimated 1.7 billion unbanked adults worldwide who have no traditional credit history but now have years of provable on-chain activity.

Emerging Markets Are the Real Growth Engine

While U.S. and European users already have Chase, Revolut, and Nubank, hundreds of millions in LatAm, Africa, Southeast Asia, and South Asia have broken or nonexistent banking systems.

For them, an on-chain neobank isn’t a crypto product—it’s simply the best banking app they’ve ever had.

Mobile-first, instant onboarding, USDC savings accounts yielding 8–12%, and zero-fee remittances beat anything available locally. Adoption curves in these regions are already parabolic.

What This Means for Investors in 2026 and Beyond

The winners of this cycle probably won’t be the most ideologically pure maximalists or the protocols with the most complex virtual machines.

The winners will be the teams that make crypto feel boring—in the best possible way.

When your mom, your driver, or your cousin in Manila uses a self-custodial wallet every single day without ever realizing it’s “crypto,” that’s when the industry finally scales.

And that’s exactly where the smart money is betting right now.

You May Also Like

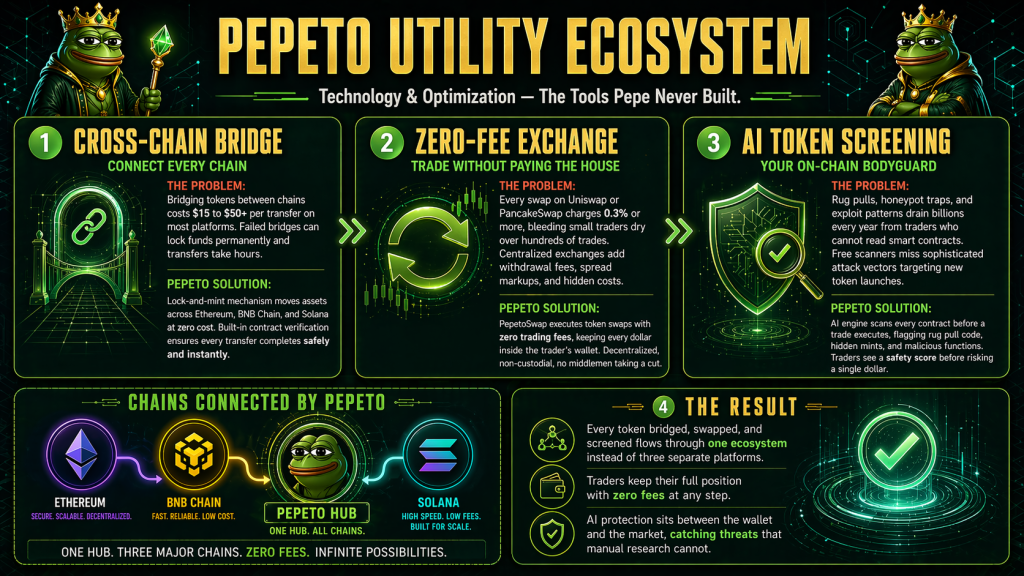

Which Are the Top 3 Cryptos to Buy Now as Solana Lands Mastercard and Pepeto Presale Nears Sold-Out Close

Ondas (ONDS) Stock Soars After Revenue Explodes Over 1,000% in Q1 2026