Can I buy crypto in Robinhood Roth IRA? A clear 2026 guide

Use this guide to compare options, understand key risks like custody and taxes, and follow a short checklist to verify whether moving funds makes sense for your situation.

Short answer: can you buy crypto in a Robinhood Roth IRA?

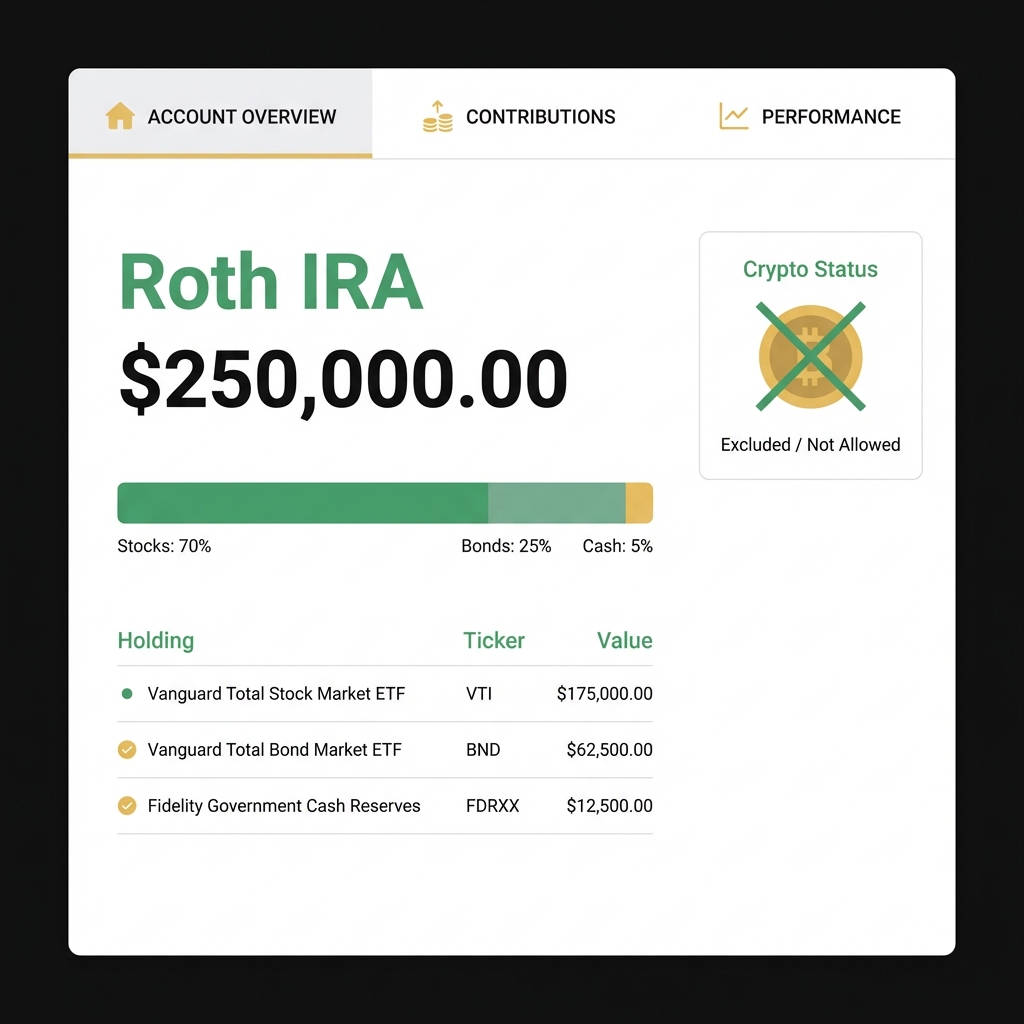

Short answer, no. Robinhood‘s publicly documented retirement accounts do not let you hold cryptocurrency directly inside a Roth IRA, based on the platform’s retirement investment listings Robinhood Help Center.

The IRS also treats virtual currency as property, which means the usual IRA tax rules apply to crypto and you should treat transfers and reporting with care.

Verify options and tax rules before you move funds

Before you act, check Robinhood's retirement investment page and consult a tax professional to confirm how rules apply to your situation.

Learn about advertising and partnership options

What it means to hold crypto inside an IRA: basic rules and players

Holding crypto inside any IRA is not simply a trading choice. The IRS treats virtual currency as property under Notice 2014-21, which affects tax treatment and record keeping for retirement accounts IRS Notice 2014-21.

That classification means crypto in an IRA follows the same retirement tax rules, but custody and documentation become more important. A self-directed IRA custodian typically handles asset custody, transaction records, and the tax forms that retirement accounts need.

Why Robinhood’s Roth IRA product doesn’t let you hold crypto directly

Robinhood lists the asset types allowed in its retirement accounts on its support pages, and that list currently excludes direct crypto holdings for Roth IRAs Robinhood Help Center.

Standard retirement platforms often limit asset types because custody, reporting, and compliance for cryptocurrencies are different from stocks and mutual funds. These operational limits can make offering direct crypto inside a Roth IRA impractical for some providers.

No. As of the latest public documentation, Robinhood's retirement accounts do not allow holding cryptocurrency directly in Roth IRAs; to hold crypto in an IRA you generally need a self-directed custodian or an IRA eligible product handled by a standard custodian.

Before assuming options exist, verify the current product terms on the custodian’s site. Platforms can change product lines, but the custody and reporting questions remain central to any change.

How crypto IRAs actually work: self-directed custodians and custody flows

To hold crypto inside an IRA you normally use a self-directed custodian that offers qualified crypto custody and retirement reporting services, which differs from standard custodians that handle only traditional securities Investopedia guide.

The usual path is: open a self-directed IRA, roll over or transfer funds from your existing IRA or 401k, then instruct the custodian to buy or custody specific crypto assets. The custodian arranges qualified custody, which may involve institutional wallets or insured third-party custody providers.

Custodians vary widely. Some use cold storage with institutional custody partners, others use on-chain wallets paired with reporting tools. Ask the custodian how custody is held, who the custody partner is, and what reports you will receive each year.

Practical workarounds: how to get crypto exposure from a Roth IRA

Option A: move retirement funds to a qualified self-directed IRA custodian that supports crypto custody. With this path you can hold actual crypto within the IRA, subject to the custodian’s custody rules, fees, and tax reporting practices Investopedia guide.

Option B: keep your Roth IRA at a standard custodian but seek IRA-eligible funds or products that provide crypto exposure indirectly. Some custodians accept certain funds or tokenized products that offer crypto exposure without direct custody of coins, though terms and availability vary.

Each workaround has tradeoffs. Direct custody via a self-directed crypto IRA can offer genuine coin ownership inside the retirement wrapper, but it often comes with higher custody fees and more complex tax reporting than indirect exposure through funds.

Fees, custody risks, and regulator warnings to consider

Investor protection groups have warned that self-directed crypto IRAs carry added custody and fraud risks compared with conventional IRAs. These warnings highlight concerns about opaque fee schedules and weaker custody practices in some offerings FINRA investor alert.

Common costs include setup fees, custody or storage fees, trading spreads, and transfer or rollover charges. These fees can meaningfully reduce long term returns, so compare fee schedules and ask for a clear summary of all costs before moving money.

Also ask about insurance and breach protection. Some custodians use institutional custody partners with insurance for certain loss events, while others disclose limited or no insurance coverage. Ask for specifics in writing and compare them across providers.

Tax and compliance checklist: UBIT, reporting, and record keeping

The IRS classification of virtual currency as property means that ordinary IRA rules apply, but certain structures can trigger unrelated business taxable income. Confirming how a custodian reports transactions is a practical first step IRS Notice 2014-21.

UBIT or unrelated business taxable income can apply when an IRA invests through operating businesses or uses leverage. Some crypto arrangements or pooled structures can create UBIT exposure, so check whether the proposed custodian or product tends to generate those tax forms.

quick verification checklist for custodian reporting and fees

Compare provider pages and ask for sample tax forms

Practical checklist items include asking the custodian whether they supply annual tax forms for retirement reporting, whether they will report transactions that could create UBIT, and whether you will receive detailed cost basis and trade history for each holding.

Typical mistakes and red flags when pursuing a crypto IRA

Avoid custodians or sales pitches that promise guaranteed returns or pressure you to move funds quickly. Those are common red flags for risky offers. Look for clear, written fee schedules and documented custody arrangements FINRA investor alert.

Other red flags include opaque custody descriptions, no insurance disclosure, and unclear tax reporting practices. If a provider will not explain how they secure assets or supply tax reports, treat that as a warning sign.

What to do next: practical steps and quick checklist

Step 1, check Robinhood’s retirement investment support page to confirm the allowed asset types for Roth IRAs before making any changes Robinhood Help Center.

Step 2, if you want direct crypto ownership, compare self-directed crypto IRA custodians for custody, fees, and reporting. Step 3, verify tax implications with IRS guidance or a tax professional before executing any rollover.

No, Robinhood's documented retirement accounts do not permit holding cryptocurrency directly in Roth IRAs. To hold crypto inside an IRA you usually need a self-directed custodian or a product the custodian accepts.

The IRS treats virtual currency as property, so IRA tax rules still apply and certain arrangements can create unrelated business taxable income. Verify reporting and consult a tax professional for your situation.

Confirm the custodian's custody arrangements, full fee schedule, insurance coverage, and tax reporting practices. Ask for sample tax forms and written custody documentation before transferring funds.

FinancePolice aims to clarify the common options and tradeoffs so you can make a more informed, cautious choice that fits your long term plan.

You May Also Like

XRP (XRP) Price Analysis: Critical Support Levels as Volatility Looms

Foreign VC exits in Kenya face 15% tax under proposed law

FTX legal adviser Fenwick settles customer lawsuit for $54m