Digital Transformation in Banking Statistics 2026: Growth, Challenges, and Opportunities

Imagine walking into a bank where there are no physical branches, no paper forms to fill out, and no waiting lines. Instead, all the services you need are available at your fingertips. That’s the reality we are rapidly moving toward as digital transformation reshapes the banking industry. Today, traditional banking models are evolving, driven by technology innovations and the growing demands of digital-first customers. This shift has sparked a wave of innovations, leading to the creation of more accessible, efficient, and customer-centric services.

In this part of the article, we will explore the major trends shaping digital banking, the rapid growth of digital platforms, mobile banking, and the significant role of Artificial Intelligence (AI) and Machine Learning (ML) in revolutionizing customer experiences.

Editor’s Choice

- 76% of U.S. adults now primarily manage their bank accounts via digital channels such as mobile apps and online platforms.

- The broader digital banking platform market size is projected to reach $43.98 billion in 2026, driven by smartphone, internet, and AI adoption.

- There are about 1.75 billion digital banking accounts globally, collectively processing roughly $1.4 trillion in transactions annually.

- Over 76% of American banking customers actively use mobile banking apps for routine financial activities.

- Digital-first transformation enables banks to cut operating costs by 20%–40% through automation and reduced reliance on branches.

- Neobank adoption is forecast to reach about 850 million users globally by 2030, according to early 2026 market projections.

Recent Developments

- The U.S. open banking market is expected to reach around $30.93 billion by 2030, expanding at a 27.9% CAGR from 2025.

- Approximately 134 countries exploring CBDCs together account for about 98% of global GDP.

- At least 72 countries are in advanced CBDC stages, such as pilot, development, or launch as of the latest assessments.

- Estonia reports over 99% of residents holding a digital ID, with roughly 70% using it regularly for services.

- Singapore’s Singpass serves more than 5 million residents, providing access to over 2,700 services from about 800 organizations.

Digital Transformation Market Growth Outlook

- The global digital transformation market is projected to grow at a strong 18.5% CAGR between 2026 and 2030.

- Market size is estimated at approximately $2,105.59 billion in 2025, reflecting already massive enterprise adoption.

- The market is expected to expand to about $2,544.35 billion in 2026, showing rapid year-over-year growth.

- Continued acceleration is forecast through the late 2020s as organizations invest heavily in cloud, AI, and automation technologies.

- By 2030, the market is projected to reach around $5,010.76 billion, more than doubling within five years.

- The steep upward trajectory highlights digital transformation as a core strategic priority across industries worldwide.

(Reference: The Business Research Company)

(Reference: The Business Research Company)

Role of Artificial Intelligence and Machine Learning

- 77% of banks worldwide invest in AI-driven insights.

- 65% of U.S. financial institutions actively deploy AI.

- 42% of U.S. institutions plan a >50% AI investment increase.

- 60-90% false positive reductions via AI fraud detection.

- AI-powered models reduce default rates by up to 25%.

- AI chatbots handle 87% of inquiries in under 60 seconds.

- 74% of AI chatbot interactions achieve first-contact resolution.

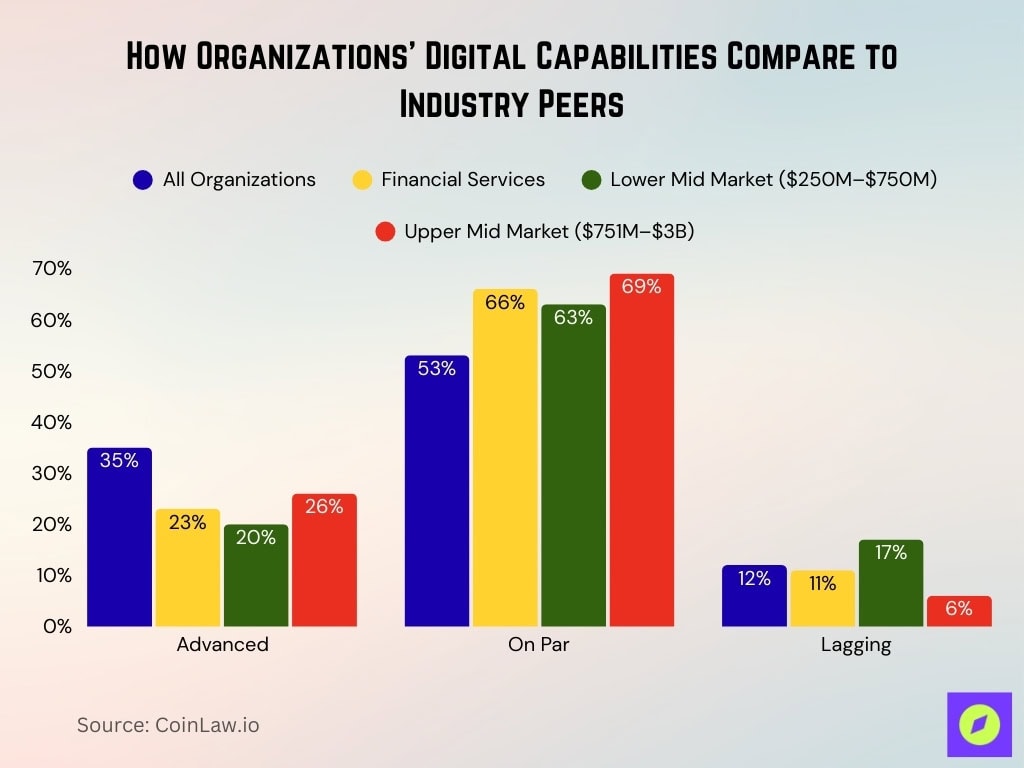

How Organizations’ Digital Capabilities Compare to Industry Peers

- Only 35% of all organizations consider their digital capabilities advanced, indicating that true digital leadership remains limited.

- Among financial services firms, just 23% report advanced capabilities, suggesting the sector faces modernization challenges despite heavy tech investment.

- In the lower mid-market segment ($250M–$750M), only 20% are advanced, the lowest among all groups analyzed.

- Upper mid-market companies ($751M–$3B) perform slightly better, with 26% achieving advanced status.

- The majority of organizations report being on par with peers, led by 69% of upper mid-market firms and 66% of financial services companies.

- Overall, 53% of all organizations say their capabilities are on par, highlighting widespread digital parity rather than differentiation.

- Lower mid-market firms also cluster in the middle, with 63% reporting on-par performance.

- A minority still lag behind: 12% of all organizations describe their capabilities as lagging.

- Financial services firms report 11% lagging, showing slightly better positioning than the overall average.

- Lower mid-market companies face the greatest risk, with 17% falling behind peers.

- Upper mid-market firms show the strongest performance, with only 6% categorized as lagging.

- Overall, the data suggests most organizations are keeping pace with competitors, but relatively few are achieving true digital leadership.

(Reference: BDO USA)

(Reference: BDO USA)

Bank’s Digital Spending Trends

- Global banks spend $1.7 trillion on digital transformation.

- Banks allocate 5% of their total budgets to AI.

- Worldwide cybersecurity spending reaches $240 billion.

- 98% of financial services organizations use cloud services.

- 82% of banks adopt hybrid or multi-cloud strategies.

- 70% of IT budgets are consumed by technical debt maintenance.

- Blockchain investments in banking hit $22.5 billion.

- $289 billion in potential benefits from scaled gen AI adoption.

- 76% of institutions need work for smart money enablement.

- 60% of banks shift 30% critical workloads to the cloud.

Digital Transformation Strategy Adoption Among Credit Institutions

- 58% of finance organizations have adopted AI as part of digital transformation.

- 75% of banks over $100 billion integrate full AI strategies.

- 86% of finance teams plan AI adoption via outsourced services.

- 98% of financial services organizations use cloud services.

- 82% of banks adopt hybrid or multi-cloud strategies.

- 94 million U.S. consumer accounts share data via open banking APIs.

- 71% of banks pursue digital transformation for lower acquisition costs.

- 68% aim to improve customer experience through digital initiatives.

- 77% of U.S. adults manage accounts via mobile or computers.

Key Drivers Behind Digital Transformation in Banking

- 71% pursue lower customer acquisition costs.

- 68% aim to improve customer banking experience.

- 68% focus on achieving top-line growth.

- 56% seek to increase operational efficiency.

- 41% driven by reaching more banked customers.

- 75% of banks invest in competitive positioning.

- 94% cite enhanced customer experiences as a driver.

- 70% motivated by faster time-to-market.

- 60% driven by cost reductions via automation.

Cybersecurity Challenges and Solutions

- 96% of the top 100 European financial institutions faced third-party security incidents.

- Average ransomware incident costs financial institutions $6.08 million.

- Global ransomware damage reaches $74 billion annually.

- 65% of financial services are hit by ransomware attacks.

- 49% of ransomware victims in finance had data encrypted.

- Worldwide cybersecurity spending hits $240 billion.

- 70% of bank executives increase cybersecurity due to AI.

- 96% of organizations account for geopolitically motivated cyberattacks.

- 40% reduction in cybersecurity response times via AI.

Top Challenges to the Employee Digital Experience (DEX)

- 37% cite security and regulatory policies as a major barrier.

- 37% overwhelmed by the number of IT issues needing resolution.

- 35% face a lack of training for IT personnel.

- 34% struggle with a hybrid or remote work shift.

- 32% challenged by increasing endpoints to manage.

- 31% say current technology is not suitable for DEX.

- 27% lack knowledge about DEX in the organization.

- 25% indicate a lack of budget for DEX efforts.

- 19% note lack of leadership buy-in for DEX.

- 41% cite tech complexity as preventing DEX priority.

Financial Inclusion Through Digital Transformation

- 1.3 billion adults are still unbanked globally.

- 55% of the unbanked live in rural areas.

- The microfinance market reaches $285.03 billion.

- Asia-Pacific holds 44.31% microfinance market share.

- 38% Nigerian adults lack SIM cards.

- 14% Indian MSMEs access formal credit.

- 60% unbanked adults have mobile phone access.

- Gender gap in account ownership narrows to 5 points.

Frequently Asked Questions (FAQs)

76% of financial institutions report needing work to enable smart money.

Around 70% of IT budgets are consumed by technical debt maintenance.

The global digitalization in the banking market is projected to reach $13.9 billion by 2026 at an 11.3% CAGR.

$13 trillion in transaction value could shift to alternative payment methods by 2030.

Conclusion

The digital transformation in banking shows no signs of slowing down. The shift from traditional to digital banking is not just a trend but a fundamental reshaping of how financial services are delivered and consumed. Artificial intelligence, cloud technology, and fintech partnerships are driving innovation, while mobile and digital banking platforms continue to expand, bringing more people into the financial system.

At the same time, banks must navigate significant challenges, particularly in the areas of cybersecurity, data privacy, and regulatory compliance. Those who can successfully integrate cutting-edge technologies while maintaining trust and security will be well-positioned to thrive in the rapidly evolving digital landscape.

The post Digital Transformation in Banking Statistics 2026: Growth, Challenges, and Opportunities appeared first on CoinLaw.

You May Also Like

Botanix launches stBTC to deliver Bitcoin-native yield

US President Donald Trump says Iran has 10 days to agree to a deal or ‘bad things happen’