Lending

Share

Lending protocols form the backbone of the decentralized money market, allowing users to lend or borrow digital assets without intermediaries. Using smart contracts, platforms like Aave and Morpho automate interest rates based on supply and demand while requiring over-collateralization for security. The 2026 lending landscape features advanced permissionless vaults and institutional-grade credit lines. This tag covers the evolution of capital efficiency, liquidations, and the integration of diverse collateral types, including LSTs and tokenized RWAs.

15505 Articles

Created: 2026/02/02 18:52

Updated: 2026/02/02 18:52

Recommended by active authors

Latest Articles

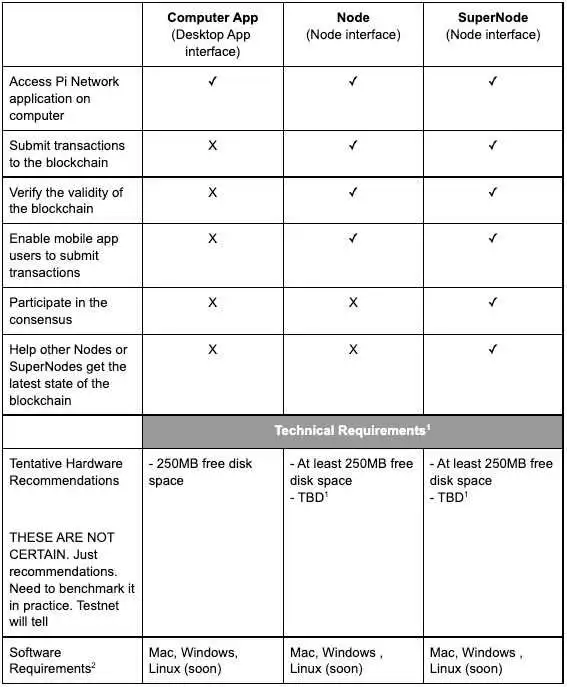

Pi Network Sets Feb 15 Deadline for Mainnet Node Upgrade

2026/02/14 04:39

Warren vs Trump’s SEC: U.S. Senate Clash Over Crypto Policy

2026/02/14 04:38

Pi Network Sets February 15 Deadline for Mandatory Mainnet Node Upgrade

2026/02/14 04:02

Singapore FY26 Budget: A Visionary Blueprint for AI-Driven Growth – MUFG Analysis

2026/02/14 03:55

Wall Street analysts slash Coinbase (COIN) price targets after Q4 miss — but shares still rally

2026/02/14 03:51